Published

Oct 27, 2025

Last Updated

Aug 5, 2026

The TSP L Income Fund: A Reliable Foundation or an Overlooked Limitation for Federal Retirees?

For many federal employees, the TSP L Income Fund is where they naturally end up as retirement approaches. It feels like the safe, logical next step a stable, hands-off fund that protects what you’ve built over your career.

But after years of helping federal employees transition from accumulation to income, we’ve learned that “safe” and “secure” aren’t always the same thing. Let’s look at how the L Income Fund works, how it’s performed, and how it fits (or doesn’t fit) into a well-structured retirement income plan.

How Is the TSP L Income Fund Performing in 2026?

As of 2026, the TSP L Income Fund continues to prioritize capital preservation and consistent income for retirees. Its allocation remains heavily weighted toward the G Fund and F Fund, with limited exposure to equities for modest growth.

In the current environment of elevated interest rates and persistent inflation pressures, the fund has generally delivered stable returns with lower volatility compared to equity-focused TSP funds. This aligns with its objective of protecting principal while providing a steady income stream.

However, because of its conservative allocation, long-term growth potential remains limited. Federal retirees relying solely on the L Income Fund should consider how inflation may impact purchasing power over time and whether additional income strategies are needed.

source - www.tsp.gov

1. Understanding the L Income Fund TSP (2025 Update)

As of October 24, 2025, the TSP L Income Fund closed at $28.9706, up 0.20% for the day.

- YTD: 8.3% | 1 Year: 8.8% | 3 Years: 9.0% | 5 Years: 6.0% | 10 Years: 5.0% | Since Inception: 4.6%

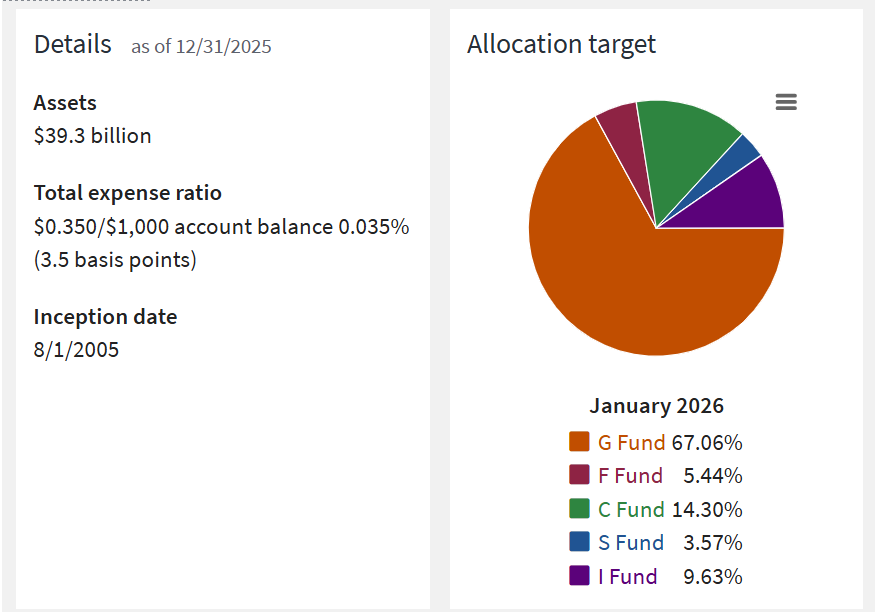

The L Income Fund is one of the five Lifecycle (L) Funds inside the Thrift Savings Plan (TSP). It’s a “fund of funds” that spreads your balance across all five core TSP options:

- 72% G Fund – Government securities

- 6% F Fund – U.S. bond index

- 11% C Fund – large U.S. stocks

- 3% S Fund – small/mid U.S. stocks

- 8% I Fund – international stocks

Unlike the other L Funds, this one doesn’t change over time it keeps a fixed allocation and is rebalanced daily to stay consistent. That means your exposure to riskier assets like stocks never drifts higher or lower.

Some investors appreciate that predictability, while others feel the fund “resets” too frequently, cutting into short-term gains. Either way, it’s designed for one clear purpose: to preserve principal and generate steady income for retirees.

With an ultra-low expense ratio of 0.042%, it’s one of the most cost-efficient, diversified options available. Since inception in 2005, the fund has earned a 4.6% compound annual return with only 4% volatility and a Sharpe Ratio of 0.45.

An initial $1,000 investment in 2005 would be worth roughly $2,495 today. The largest historical drawdown was about –11% during the 2008 crisis a fraction of what the stock market lost. Before choosing the L Income Fund for retirement income, it’s important to understand the when can you withdraw from TSP without penalty, as timing directly impacts how and when you can access your funds.

To better estimate how your TSP balance may grow and support your retirement income strategy, you can use a TSP growth calculator to model different scenarios based on contributions, returns, and withdrawal timing.

2. What the Numbers Mean for Retirees

The L Income Fund’s steady performance reflects its purpose: protect capital, smooth volatility, and generate modest income. But for retirees depending on their TSP for 25 or 30 years, modest growth can become a long-term limitation.

In our experience working with federal retirees, we often see this pattern: someone moves everything into the L Income Fund thinking it’s the “final destination.” Ten years later, inflation has quietly reduced their spending power, and their withdrawals are beginning to erode their balance faster than expected.

That’s the key trade-off stability today versus purchasing power tomorrow

3. The Real Risk: Inflation and Opportunity Cost

Many retirees underestimate inflation risk especially after decades of focusing on market risk. While the L Income Fund rarely swings more than a few percent, it also struggles to stay ahead of rising prices over time.

If inflation averages 3% per year and your fund grows around 4–5%, your real return is barely positive. Over a long retirement, that can make a big difference in lifestyle.

In our experience, the most successful federal retirees don’t eliminate risk; they manage it. They hold enough stable assets for short-term income needs, but they keep part of their portfolio growing to maintain purchasing power down the road.

4. When the L Income Fund Works Well

The fund can be an excellent fit for certain goals and timelines:

- You’re already retired and drawing monthly income from TSP.

- You prefer capital preservation over higher returns.

- You want a hands-off fund that stays automatically balanced.

We often recommend it as the “income bucket” in a broader strategy. For example, one client a recently retired GS-13 with a $700,000 TSP balance keeps about five years of expected withdrawals in the L Income Fund. The rest remains invested in growth-oriented L Funds (L 2030 and L 2040).

This structure gives her the confidence that near-term income is protected, while the remaining funds continue to outpace inflation.

Many federal employees who retire early rely on the TSP Rule of 55 for early retirement to begin withdrawals without penalties, making it a key strategy when using the L Income Fund for income.

5. When It May Be Too Conservative

If you’re more than a few years from retirement or expect a 25+ year retirement the L Income Fund alone may be too conservative.

- Inflation risk: The fund’s heavy G Fund exposure limits growth, especially during high inflation.

- Sequence risk: Even small declines during withdrawals can compound over time.

- Longevity: Returns near 4–5% may not sustain a 30-year income plan without supplemental growth assets.

In our experience, federal employees who rely solely on the L Income Fund often find themselves revisiting their strategy later, once they see their balance flattening while expenses rise. Remeber that you should check once that if you can withdraw money from my tsp before you retire or not.

6. Advisor Perspective: Building a Smarter Income Strategy

The L Income Fund isn’t a mistake it’s a tool. The key is using it in the right proportion.

A well-structured retirement plan goes beyond fund selection it requires understanding how FERS, TSP, and Social Security work together in retirement to create a sustainable income strategy.

Here’s a common framework we build for clients transitioning into retirement:

This layered approach helps protect near-term withdrawals while still keeping part of your portfolio growing for future needs. We also coordinate this with FERS annuity and Social Security timing so that your income stream remains predictable regardless of market conditions.

In our experience, this balance not overreacting to markets, but not sitting entirely in cash produces the most stable retirements over time.

7. Key Takeaways

- The TSP L Income Fund provides steady returns and low volatility, averaging around 4–5% long-term.

- It’s ideal for short-term income stability, but not designed for inflation protection.

- Consider using it as one layer of a diversified retirement income plan not as the entire strategy.

- A thoughtful mix of safety and growth can extend your income and safeguard your lifestyle for decades.

Must to read - how to withdraw from tsp while in service

Next Step: Let’s Review Your TSP Plan Together

If you’re approaching retirement or already drawing from your TSP, now is the time to make sure your allocation truly supports your income goals not just your comfort level.

Our team specializes in helping federal employees and retirees build clear, inflation-aware TSP income strategies. We’ll help you determine how much to keep in the L Income Fund, when to adjust, and how to balance security with sustainable growth.

Schedule a complimentary TSP review today and make sure your “safe” choice is also your smartest one.

FAQs

What are the disadvantages of an income fund?

Income funds can experience interest rate risk, where rising rates decrease value; credit risk, from lower-rated bonds that could default; and market volatility, meaning returns fluctuate and may not be guaranteed. They also may charge fees that lower overall returns and are not entirely risk-free, particularly with funds that include equities.

What is the best fund to put my TSP in?

The best TSP fund depends on your career stage and risk tolerance:

- Young investors: Favor growth with more in C, S, and I Funds (stocks, both U.S. and international).

- Mid-career: Consider a balanced mix including some G and F Funds for stability.

- Near retirement: Prioritize safety, typically with a higher allocation to the G Fund (government securities).

Lifecycle (L) Funds offer automatic rebalancing for hands-off investors but may dilute returns compared to aggressive stock allocations.

What is the rate of return on the TSP fund?

TSP fund returns vary each year and by fund type:

- G Fund: About 4.25% to 4.625% annually in 2025, stable but lower growth.

- C, S, and I Funds: Stock funds exhibit much higher variability recent years have seen C Fund returns average over 10%, S Fund near 9%, and I Fund around 5%, but these fluctuate in any given year.

- L Funds: These reflect blended rates, matching their component funds and glide path.

Sources

Federal News Network

Descliamer

The information provided in this article is for educational and informational purposes only and should not be considered financial, investment, or retirement advice. The examples and scenarios are for illustration and do not represent specific client outcomes.

Past performance of the TSP L Income Fund or any Thrift Savings Plan investment option does not guarantee future results. Investment returns and principal value may fluctuate, and you could lose money by investing.

Get Updated

Subscribe to our weekly updates for the latest on retirement planning, federal benefits, exclusive webinars, and more!

Download Federal Retirement: Step-by-step Checklist

This comprehensive guide will help you understand your federal benefits, optimize your savings, and plan for a comfortable future.