.png)

TSP In-Plan Roth Conversion 2026: Rules, Taxes, and When It Makes Sense

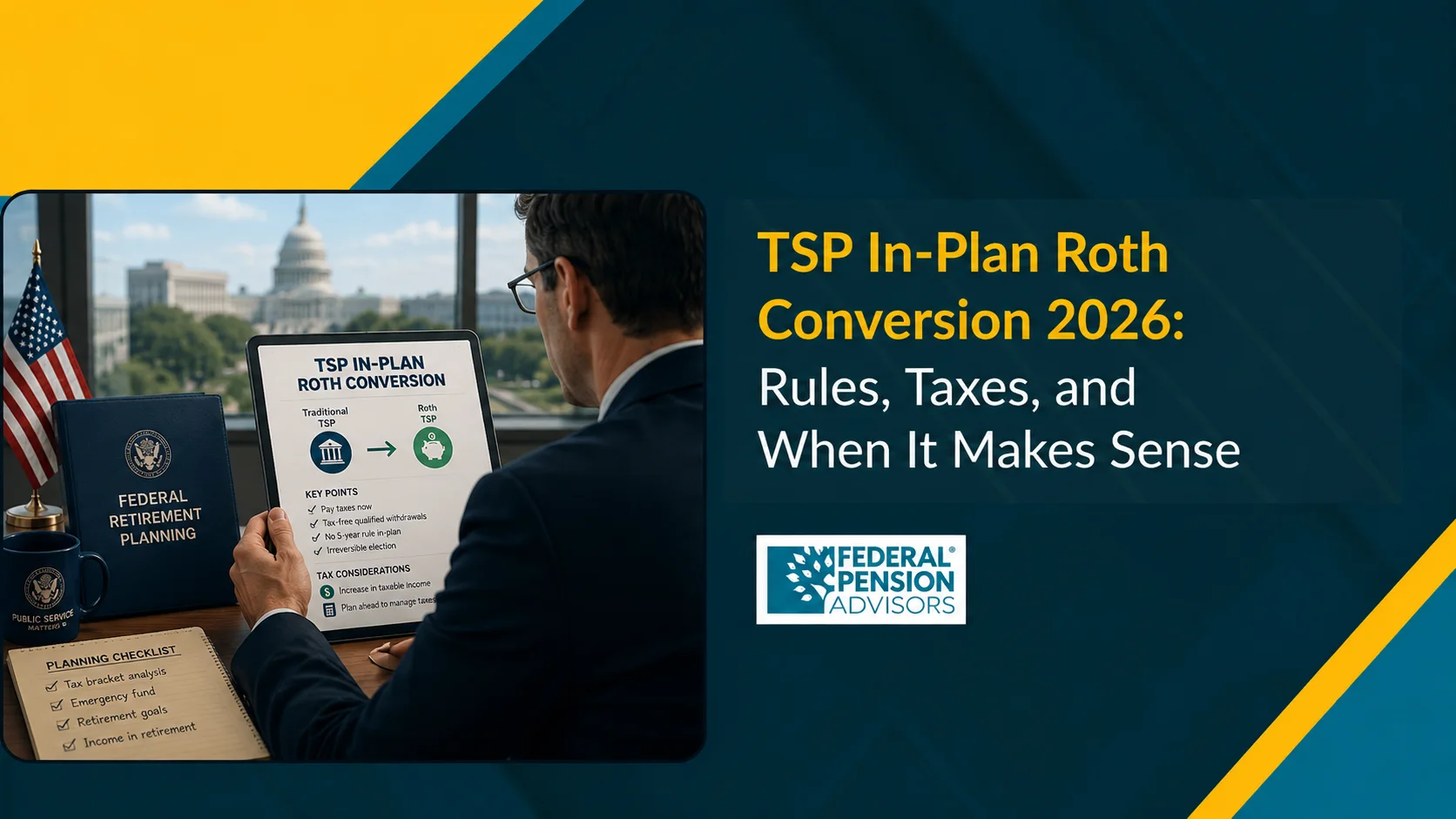

A TSP in-plan Roth conversion moves money from your traditional TSP balance directly into your Roth TSP balance without taking the money out of the plan. You pay ordinary income tax now. In return, you get tax-free growth and tax-advantaged withdrawals later.

In 2026, eligible TSP participants can convert money from a traditional TSP balance to a Roth TSP balance inside the plan. This guide explains the current rules, the tax mechanics, and the specific circumstances in which a TSP Roth conversion in 2026 makes financial sense.

What Is a TSP In-Plan Roth Conversion?

A TSP in-plan Roth conversion lets you transfer all or part of your traditional TSP balance, including tax-deferred employee contributions, agency matching contributions, and earnings, into your Roth TSP balance. The converted amount counts as ordinary taxable income in the year of conversion.

Once inside the Roth TSP, your money grows tax-deferred. Qualified withdrawals in retirement are generally tax-free when IRS distribution requirements are met.

This differs from a rollover to a Roth IRA. With an in-plan conversion, the money never leaves the TSP. You keep access to the TSP's institutional fund expense ratios, which the Federal Retirement Thrift Investment Board notes are among the lowest available in any retirement savings vehicle.

That cost advantage is one reason many federal employees prefer converting inside the plan rather than rolling assets out. Under FERS, most employees can access in-plan Roth conversion through their TSP account interface. Employees covered by CSRS who still hold active TSP balances are also eligible.

TSP Roth Conversion Rules in 2026

Before you act, you need to know what can be converted, when, and what triggers a tax liability.

What balances are eligible for conversion

Not every dollar in your TSP qualifies. According to the Federal Retirement Thrift Investment Board, the following balances are eligible for TSP in-plan Roth conversion in 2026:

- Traditional employee contributions and their earnings

- Agency automatic (1%) contributions and their earnings

- Agency matching contributions and their earnings

- Rolled-over traditional IRA or 401(k) balances previously moved into the TSP

Not eligible for in-plan conversion: Required Minimum Distributions (RMDs), outstanding TSP loan balances, and any amounts already designated as Roth contributions.

Vesting requirements

Agency automatic contributions, the 1% automatic contribution under FERS, must be fully vested before you can convert them. Under FERS, the standard vesting period for automatic contributions is three years of federal civilian service, or two years for certain special category employees. Agency matching contributions vest immediately.

Age and separation status

You don't need to be separated from federal service to complete a Roth in-plan conversion. If you're under age 59½ at the time of conversion, the converted amount added to your income does not trigger the 10% early withdrawal penalty. The money stays inside the TSP. The only immediate consequence is the income tax owed on the converted amount.

The five-year rule

Roth TSP withdrawals must satisfy the applicable five-taxable-year rule and qualified distribution requirements to receive tax-free treatment on earnings. According to IRS guidance on designated Roth accounts, nonqualified distributions may cause the earnings portion to be taxable. Verify how the five-year rule applies to your specific converted amounts before withdrawing Roth TSP earnings, particularly if you've made multiple conversions in different years.

How the Taxes Work on a Traditional TSP to Roth TSP Conversion

The tax mechanics of a traditional TSP to Roth TSP conversion are straightforward but easy to underestimate. The full converted amount is added to your ordinary income for the year of conversion. There's no special capital gains rate, no averaging, and no deferral.

Example calculation

Suppose a FERS employee earns a gross salary of $85,000 in 2026 and converts $20,000 from their traditional TSP. Their taxable income before deductions becomes $105,000. Under 2026 single-filer brackets, that amount stays within the 22% bracket, since the 24% bracket doesn't begin until income exceeds $105,700. A slightly larger conversion could push income into the next bracket. State income taxes apply in most states and must be factored in separately.

Planning note: Pay the tax on a conversion from outside your retirement savings if you can. Using TSP funds to cover the tax bill reduces the amount benefiting from tax-free growth. If you're under age 59½, the TSP withdrawal used to pay taxes is itself a taxable distribution that may carry additional consequences.

2026 federal income tax brackets (relevant range)

Source: IRS, "IRS releases tax inflation adjustments for tax year 2026, including amendments from the One Big Beautiful Bill," IRS.gov.

Married filing jointly thresholds are double the single-filer amounts at the lower brackets. Use the IRS.gov tax withholding estimator or a tax professional to model your specific scenario before converting.

Traditional TSP vs. Roth TSP: Key Differences

Your conversion decision starts with understanding how the two account types work.

Source: TSP Bulletin 25-3, Federal Retirement Thrift Investment Board, 2026 contribution limits.

Under SECURE 2.0, Roth TSP balances are no longer subject to RMDs starting in 2024. That's a significant advantage for estate planning and tax control in later retirement years, and one more reason to model whether a conversion fits your situation.

TSP Tax Planning 2026: When a Roth Conversion Makes Sense

A TSP in-plan Roth conversion isn't the right move for every federal employee. The decision depends on your current tax rate versus your projected tax rate in retirement, your time horizon, and your broader TSP tax planning goals for 2026.

Scenario 1: You're in a low tax year

If your income is temporarily lower in 2026, due to a career transition, leave without pay, part-time status, or a gap between federal jobs, your marginal tax rate may be lower than it will be in retirement. Converting during a low-income year locks in that lower rate. Federal employees who retired mid-year and have a partial income year often find this the most compelling window for a conversion.

Scenario 2: You want to plan around future tax rate changes

For 2026 planning, use the current IRS tax brackets and confirm whether future tax law changes could affect your long-term Roth conversion strategy. Federal Pension Advisors recommends modeling conversion scenarios under current-law rates as well as potential future rate environments before committing to a conversion amount. Explore TSP tax planning strategies for federal employees to see how different rate scenarios affect your outcome.

Scenario 3: You have a long runway before retirement

The longer your converted balance has to grow tax-free, the more valuable Roth treatment becomes. A federal employee who is 15 or more years from retirement and converts a $50,000 traditional balance today gives that money a decade and a half to compound without future tax drag. The breakeven point, where tax-free growth offsets the upfront tax paid, arrives faster the longer the holding period.

Scenario 4: You want to reduce future RMDs

Traditional TSP balances are subject to Required Minimum Distributions starting at age 73 under SECURE 2.0. Large traditional TSP balances can produce RMDs that push retirees into higher tax brackets, trigger Medicare IRMAA surcharges, and increase the taxability of Social Security benefits. According to the Social Security Administration, up to 85% of Social Security benefits can become taxable when combined income exceeds certain thresholds. Reducing your traditional TSP balance through strategic in-plan conversions before age 73 can meaningfully lower future RMD-driven tax exposure.

Scenario 5: You're in the 12% bracket with headroom

Federal employees whose total income falls in the 12% bracket can convert up to the top of that bracket at a relatively low tax cost. For a single filer in 2026, that ceiling is $50,400 of taxable income. Converting enough to fill the bracket without crossing into 22% territory is a classic federal Roth conversion in 2026 strategy recommended by retirement planning professionals. Learn how bracket-filling conversions work in practice.

When a TSP Roth Conversion May Not Make Sense

A federal employee Roth conversion isn't always the right call. A conversion may not make sense in these situations:

- You'll retire within one to three years and expect significantly lower income in retirement. Your retirement tax rate may be lower than your working-year rate, making a conversion counterproductive.

- You can't pay the tax from outside the TSP. Using TSP funds to cover the tax bill undermines the math of the conversion.

- The conversion would trigger IRMAA. If you're already on Medicare or approaching Medicare age, a large conversion can increase your Part B and Part D premiums for two years through IRMAA income-related adjustments.

- You're in a high-income year with no flexibility. Converting when income already sits near the 32% or 35% bracket substantially reduces the long-term benefit.

How to Execute a TSP In-Plan Roth Conversion in 2026

The process runs entirely through the TSP website.

- Log in to TSP.gov using your account credentials.

- Navigate to "Manage My Account" and select the in-plan Roth conversion option under the transactions menu.

- Select the amount you want to convert. Choose a specific dollar amount or a percentage of your eligible traditional balance.

- Confirm fund allocation. The converted amount moves into your Roth TSP and invests according to your existing Roth TSP allocation. Update your allocation first if needed.

- Acknowledge the tax notice. The TSP requires you to confirm you understand the tax consequences before completing the transaction.

- Adjust your withholding. Consult your tax professional and update your federal withholding or estimated tax payments to account for the added income. Use IRS Form W-4 to increase withholding from your paycheck if needed.

Complete in-plan conversions earlier in the calendar year when possible. Converting in December makes it difficult to adjust withholding adequately and can result in underpayment penalties.

Is a TSP Roth Conversion Right for You in 2026?

A TSP in-plan Roth conversion in 2026 is a strong tax planning move for federal employees who are currently in a lower tax bracket than they expect in retirement, who have enough non-TSP assets to cover the tax liability, and who have enough time for tax-free growth to offset the upfront cost.

The elimination of RMDs on Roth TSP balances under SECURE 2.0, combined with potential future tax rate changes, makes 2026 a strategically relevant year to model a conversion scenario. Your decision requires modeling your specific income, bracket position, retirement timeline, FERS annuity projection, and Social Security benefit. There's no universal answer, only the answer that fits your individual federal retirement picture.

Schedule a consultation with a federal retirement specialist at Federal Pension Advisors to model your TSP Roth conversion scenario and get a personalized FERS retirement analysis.

Frequently Asked Questions

1. When can I do a TSP in-plan Roth conversion?

Active federal employees with a traditional TSP balance can perform an in-plan Roth conversion at any time through TSP.gov, regardless of age or years of service. The converted amount counts as taxable income in the year of conversion. Vested balances, including agency automatic contributions after three years, are eligible. According to TSP.gov, participants may make up to 26 Roth in-plan conversions per calendar year.

2. How is a TSP in-plan Roth conversion taxed in 2026?

The full converted amount is added to your ordinary taxable income in the year of conversion and taxed at your applicable federal marginal rate. According to the IRS, 2026 brackets range from 10% to 37%. No 10% early withdrawal penalty applies because the money stays inside the TSP. State income taxes may also apply depending on your state of residence.

3. Can I convert my TSP to a Roth IRA instead of using in-plan conversion?

Yes. If you're separated from federal service, you can roll your traditional TSP balance directly to a Roth IRA, which also triggers income tax on the converted amount. Active employees can't roll TSP funds out while still employed. The in-plan conversion keeps the money inside the TSP and preserves access to the plan's low-cost institutional funds.

4. Does a TSP Roth conversion affect my FERS pension?

No. Your FERS annuity is calculated based on your High-3 average salary and your years of service. TSP account activity, including Roth conversions, has no effect on your FERS annuity calculation. See how your High-3 and years of service determine your FERS pension.

5. What is the five-year rule for TSP in-plan Roth conversions?

Roth TSP withdrawals must satisfy the applicable five-taxable-year rule and IRS qualified distribution requirements to receive tax-free treatment on earnings. According to IRS guidance on designated Roth accounts, nonqualified distributions may cause the earnings portion to be taxable. Verify how the five-year rule applies to your converted amounts before making Roth TSP withdrawals.

6. Should I convert my entire traditional TSP balance at once?

Rarely. Converting your entire traditional TSP balance in a single year typically pushes a large amount of income into high tax brackets, reducing the efficiency of the strategy. Most financial planners recommend a multi-year partial conversion strategy, converting enough each year to fill a lower bracket without crossing into the next.

Disclaimer

This article is for informational purposes only and does not constitute tax, legal, investment, or financial advice. TSP Roth conversion rules, tax brackets, RMD rules, and Medicare IRMAA thresholds may change. Federal employees should consult a qualified tax professional or financial advisor before making Roth conversion decisions.

Get Updated

Subscribe to our weekly updates for the latest on retirement planning, federal benefits, exclusive webinars, and more!

Michael A. Fox

Michael A. Fox is a seasoned Financial Advisor and Retirement Income Planning Specialist with more than 25 years of experience helping individuals and families make informed retirement decisions. His focus is on retirement income planning, protection strategies, and helping clients build long-term financial confidence through clear, practical guidance.

Download Federal Retirement: Step-by-step Checklist

This comprehensive guide will help you understand your federal benefits, optimize your savings, and plan for a comfortable future.