Published

Nov 18, 2025

Last Updated

Dec 11, 2025

Difference Between Rollover and Transfer for Federal Employees (Direct Rollover vs Transfer Explained)

If you’ve ever tried to move your retirement savings, you’ve probably run into confusing terms like transfer, rollover, direct rollover, and direct transfer.

For federal employees and retirees, understanding the difference between rollover and transfer is more than just jargon it’s about avoiding unnecessary taxes, penalties, or delays when you move your Thrift Savings Plan (TSP), IRAs, or old employer plans.

In this guide, we’ll walk through:

- What a transfer is

- What a rollover is

- The key differences in tax treatment, paperwork, and risk

- How direct rollover vs transfer works in real life for federal employees

- Practical examples, decision points, and common mistakes to avoid

What Is the Difference Between Rollover and Transfer?

At a high level, here’s the simple version:

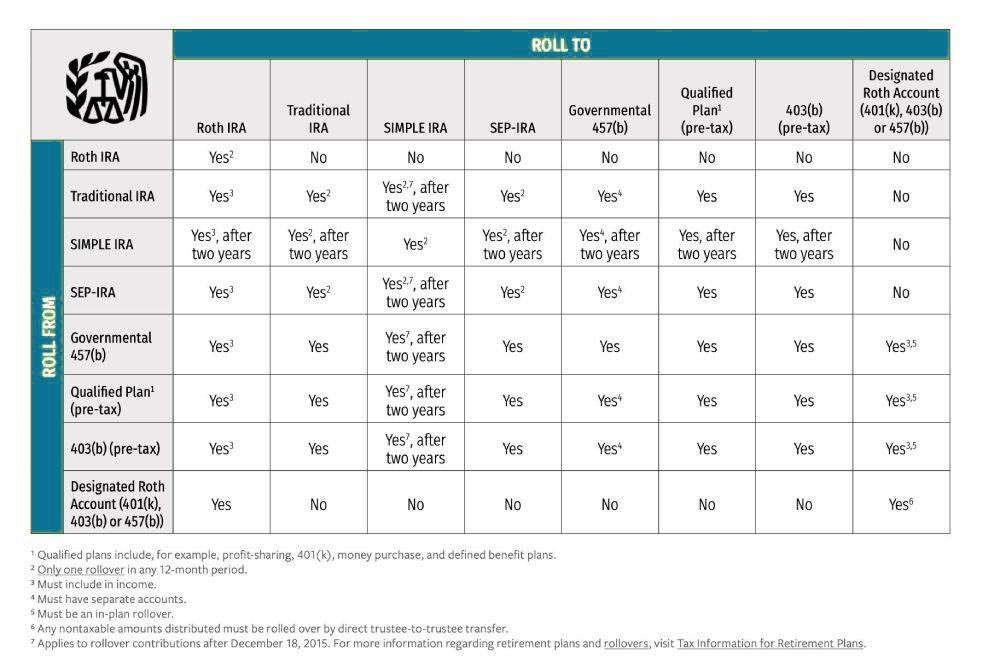

- A transfer moves money between the same type of retirement account (for example, Traditional IRA to Traditional IRA), usually between two financial institutions.

- A rollover moves money from one kind of retirement plan to another, like a TSP or 401(k) into an IRA.

When people search for the difference between rollover and transfer, they’re usually trying to answer questions like:

- “If I’m leaving federal service, should I roll over my TSP or transfer something else?”

- “Is it safer to do a direct transfer vs rollover?”

- “What’s the best option for me: direct rollover vs transfer?”

We’ll break it down methodically, starting with the simpler one: transfers.

What Is a Transfer? (Direct Transfer vs Rollover Basics)

Definition of a Transfer

A transfer is a direct movement of funds between two accounts of the same type, held at different financial institutions or custodians.

Examples:

- Traditional IRA at Bank A → Traditional IRA at Brokerage B

- Roth IRA at Provider X → Roth IRA at Provider Y

This is sometimes called a trustee-to-trustee transfer or custodian-to-custodian transfer. The key is:

- The money is made payable to the new custodian, not to you.

- You never receive the money personally.

- The account type stays the same.

This is why, in the direct transfer vs rollover conversation, transfers are usually considered the cleanest, safest move when you’re staying within IRA territory.

When Do People Use Transfers?

You might use a transfer when:

- You want better investment choices than your current IRA provider offers.

- You’re consolidating multiple IRAs into one account for simplicity.

- You’re unhappy with service, technology, or fees at your current custodian.

- You’re working with an advisor or firm (like Federal Pension Advisors) who recommends a different IRA platform.

Transfers are especially helpful for federal employees who:

- Accumulated several IRAs over multiple jobs or years.

- Want to simplify before retirement or before RMDs start.

Want to better coordinate their IRA strategy with TSP and federal benefits.

How Transfers Work (Step by Step)

Here’s how a typical direct transfer vs rollover process looks on the transfer side:

- Open the new IRA at your chosen institution (if you don’t already have one).

- Complete a transfer form with the new institution. They often coordinate directly with the old custodian.

- The funds move directly from old custodian to new custodian—often as cash, sometimes in-kind (you may be able to transfer certain investments without selling them).

- Your old IRA closes or remains open with a lower balance, depending on what you request.

No check payable to you. No 60-day clock. No stress.

Tax and Reporting Treatment of Transfers

This is a major reason transfers are so popular:

- No taxes withheld

- No early withdrawal penalties

- Not treated as a distribution

- Generally not reported to the IRS as a taxable event

You can do unlimited transfers per year. There’s no annual limit on the number or size of transfers.

When clients ask us about rollover vs direct transfer from IRA to IRA, the tax simplicity of transfers usually tips the scales in favor of a transfer if the account types are the same.

Special Rules and Exceptions

A few nuances:

- SIMPLE IRAs can be transferred to a Traditional IRA only after two years from the date of the first contribution.

- Inherited IRAs have their own special rules transfers are often allowed, but rollovers usually are not.

- RMDs (Required Minimum Distributions) cannot be transferred or rolled over. They must be taken as distributions.

What Is a Rollover? (Rollover vs Direct Transfer in Action)

Definition of a Rollover

A rollover happens when you move money from one type of retirement plan into another, often from an employer plan into an IRA.

Common examples:

- TSP → Traditional IRA

- TSP → Roth IRA (taxable conversion)

- 401(k) → Traditional IRA

- 403(b) → Traditional IRA

When people search “difference between rollover and transfer,” they’re often just left a job or are retiring from federal service and want to know what to do with:

- An old TSP balance

- A previous employer’s 401(k)

- Multiple workplace plans accumulated over time

All rollovers require IRS reporting, but not all rollovers are taxed. That depends on how you do it.

Also read - what is a 401a retirement plan

Two Main Types of Rollovers

When comparing direct transfer vs rollover, it’s useful to break rollovers into two types: direct and indirect.

1. Direct Rollover (Direct Rollover vs Transfer)

A direct rollover is often the preferred option when moving money from an employer plan (like the TSP) into an IRA.

What happens:

- The funds move directly from your employer plan to your IRA.

- The check is payable to the new institution (e.g., “XYZ Brokerage FBO John Smith IRA”), not to you.

- No mandatory tax withholding.

- No 60-day deadline applies to you personally, because you never take possession of the funds.

This makes direct rollover vs transfer very similar from a risk standpoint: both are custodian-to-custodian and avoid unnecessary taxes and timing pressure. The difference is what you’re moving (employer plan → IRA in a rollover, vs IRA → IRA in a transfer).

2. Indirect Rollover (60-Day Rollover)

An indirect rollover is a different animal.

Here’s what happens:

- The plan or IRA issues the distribution to you personally.

- For employer plans (like TSP, 401(k), 403(b)), 20% must be withheld for federal taxes.

- For IRAs, the default withholding is often 10%, unless you opt out.

- You then have 60 days from the date you receive the funds to deposit the full amount into another retirement account.

Why is this risky?

- You must come up with the withheld amount from your own pocket to avoid tax on that withheld portion.

- If you miss the 60-day deadline, the entire distribution is taxable, and if you’re under 59½, it may also be subject to a 10% early withdrawal penalty.

- For IRAs, you can only do one indirect rollover every 12 months (across all your IRAs), which is a huge difference when thinking about direct transfer vs rollover rules.

Because of these pitfalls, we usually recommend federal employees use direct rollovers, not indirect rollovers, whenever possible.

How Rollovers Work in Practice for Federal Employees

Let’s look at a few situations.

Example 1: Retiring Federal Employee – TSP to IRA

You retire from federal service and want more investment flexibility than the TSP offers.

You choose a direct rollover:

- Open a Traditional IRA at your chosen institution.

- Complete the TSP forms to do a direct rollover into that IRA.

- The TSP sends the funds directly to the IRA custodian.

Result:

- No taxes withheld.

- No 60-day rule.

- The transaction is reported, but not taxed.

This is a classic direct rollover vs transfer situation. You’re not allowed to “transfer” TSP money into an IRA that movement is technically a rollover, even though it feels similar to a transfer.

Example 2: Old 401(k) from Private Employment → IRA While You’re a Federal Employee

You previously worked in the private sector and still have a 401(k) sitting at your old employer’s plan.

You can:

- Use a direct rollover from the 401(k) to a Traditional IRA.

- Or, if you’re eligible and it fits your strategy, roll that 401(k) into the TSP instead.

Again, this is rollover vs direct transfer in action because we’re moving between plan types.

Direct Rollover vs Transfer: Side-by-Side Comparison

To really see the difference between rollover and transfer, it helps to look at them together.

High-Level Comparison

Where People Get Confused: Rollover vs Direct Transfer

When people talk about rollover vs direct transfer, they often use the terms casually:

- “I’m transferring my 401(k) to an IRA” (technically a direct rollover, not a transfer).

- “I rolled over my IRA to another IRA” (technically a transfer, unless money passed through your hands).

For SEO purposes, we use both phrases rollover vs direct transfer and direct transfer vs rollover but the underlying distinction is still:

- Same account type → transfer

Different plan types → rollover

Decision Framework: When to Use Transfer vs Rollover

When deciding between direct rollover vs transfer, start with a few questions.

1. Are You Moving an IRA or an Employer Plan?

- If you’re moving IRA to IRA (Traditional to Traditional, Roth to Roth), that’s typically a transfer.

- If you’re moving TSP or 401(k) to IRA, that’s a rollover ideally a direct rollover.

2. Do You Want to Avoid Withholding and Deadlines?

If your priority is to avoid any chance of:

- Tax withholding

- Missing a 60-day rollover deadline

- Triggering the one-per-year rollover limit on IRAs

Then:

- Choose an IRA transfer instead of an indirect rollover.

- Choose a direct rollover instead of an indirect rollover from an employer plan.

In the direct transfer vs rollover debate, it’s less about the label and more about whether the funds ever pass through your hands. If they don’t, you’re usually safer. This may help direct rollover vs 60 day rollover.

3. Are You a Federal Employee or Retiree With TSP?

You’ll likely use:

- Direct rollover when moving TSP → IRA.

- Transfer when consolidating existing IRAs at different institutions.

In practice, many federal retirees do both:

- Direct rollover from TSP to IRA.

Transfers between IRAs to unify everything at one custodian.

Logistics, Timing, and Common Pitfalls

How Long Does a Transfer or Rollover Take?

Timelines vary by institution:

- Transfers (IRA → IRA): Often 3–10 business days, depending on the custodians, how the assets are sent (check vs electronic), and whether assets must be sold first.

- Direct rollovers (TSP/401(k) → IRA): Often 1–3 weeks, especially if paper forms are required or if the plan cuts physical checks.

Fees and Market Impact

Be aware of:

- Outgoing transfer or closure fees at some institutions.

- Trading or transaction fees when liquidating or reinvesting.

- Potential market timing risk if your investments are sold to cash and reinvested later at different prices.

This is another reason it helps to have guidance when deciding between rollover vs direct transfer.

Pitfalls to Avoid

No matter how you move your accounts, watch out for these common mistakes:

- Having the check made payable to you instead of the new custodian

- This turns a simple direct rollover into an indirect rollover with withholding and a 60-day clock.

- This turns a simple direct rollover into an indirect rollover with withholding and a 60-day clock.

- Missing the 60-day deadline on an indirect rollover

- The full amount becomes taxable, plus possible penalties if you’re under 59½.

- The full amount becomes taxable, plus possible penalties if you’re under 59½.

- Not replacing the withheld amount on an indirect rollover

- If your old plan withholds 20% and you only redeposit 80%, the 20% is treated as a taxable distribution.

- If your old plan withholds 20% and you only redeposit 80%, the 20% is treated as a taxable distribution.

- Trying to roll over an RMD

- RMDs cannot be rolled over. Any attempt to do so will create tax headaches.

- RMDs cannot be rolled over. Any attempt to do so will create tax headaches.

- Violating the one-per-year rule on indirect IRA rollovers

- You can only do one indirect IRA-to-IRA rollover in a 12-month period, regardless of how many IRAs you own.

This rule does not apply to transfers or to direct rollovers from employer plans.

- You can only do one indirect IRA-to-IRA rollover in a 12-month period, regardless of how many IRAs you own.

Tax and Reporting: How the IRS Sees Rollover vs Direct Transfer

Transfers

- Transfers are usually non-reportable events for you.

- The IRS does not see them as taxable distributions or contributions.

- No Forms 1099-R or 5498 are triggered just for a simple IRA-to-IRA transfer.

Rollovers

- The sending institution issues a Form 1099-R reporting the distribution.

- The receiving institution issues a Form 5498 reporting the rollover contribution.

- On your tax return, you may need to indicate that the distribution was rolled over and is not taxable (for example, writing “rollover” on the appropriate line if required).

This is where the difference between rollover and transfer becomes more than semantic rollovers create paperwork and possible tax implications, transfers generally do not.

How This Fits Your Overall Federal Retirement Strategy

Federal employees have a unique mix of benefits:

- TSP

- FERS or CSRS pension

- Social Security (for most)

- Possibly private IRAs, 401(k)s, or 403(b)s from previous employment

When you understand direct rollover vs transfer, you can:

- Consolidate old accounts efficiently.

- Avoid unnecessary taxes or penalties.

- Simplify RMDs later by having fewer accounts.

- Coordinate TSP decisions with IRA and pension planning.

In many cases, a federal retiree’s path looks like:

- Direct rollover from TSP into an IRA for more flexibility.

- Transfers between IRAs to consolidate everything at one custodian.

- Strategic decisions about future Roth conversions and withdrawal order.

Key Takeaways on Difference Between Rollover and Transfer

- The difference between rollover and transfer starts with what you’re moving:

- Same account type → usually a transfer.

- Employer plan to IRA → usually a rollover.

- Same account type → usually a transfer.

- Direct transfer vs rollover isn’t about which is “better”; it’s about:

- Whether funds stay in IRAs or move out of an employer plan, and

- Whether the money ever passes through your hands.

- Whether funds stay in IRAs or move out of an employer plan, and

- Direct rollover vs transfer:

- Both avoid withholding and 60-day deadlines when done correctly.

- Both move money directly between institutions.

- Rollovers are reported to the IRS; transfers typically are not.

- Both avoid withholding and 60-day deadlines when done correctly.

- Indirect rollovers involve more risk:

- Withholding, strict 60-day deadline, and one-per-year rule for IRAs.

For most federal employees, the goal is simple: use direct rollovers and transfers to move money cleanly, avoid tax surprises, and keep the long-term plan intact.

- Withholding, strict 60-day deadline, and one-per-year rule for IRAs.

FAQs: Rollover vs Direct Transfer for Federal Employees

1. What is the main difference between rollover and transfer?

A transfer moves money between the same types of retirement accounts (like IRA to IRA), typically without IRS reporting or tax consequences.

A rollover moves money from one plan type to another (like TSP or 401(k) to IRA) and is reportable, but not necessarily taxable if done correctly.

2. Is moving my TSP to an IRA a transfer or a rollover?

Moving your TSP to an IRA is a rollover, specifically a direct rollover if done custodian-to-custodian. The TSP is an employer plan; IRAs are individual accounts, so this falls on the rollover side of the rollover vs direct transfer conversation.

3. How many transfers can I do in a year?

There is no limit on the number of IRA transfers you can complete in a year.

The one-per-year rule applies only to indirect IRA rollovers, not to transfers or direct rollovers from employer plans.

4. Can I roll over or transfer my RMD?

No. Required Minimum Distributions (RMDs) cannot be rolled over or transferred. They must be taken as taxable distributions.

5. Which is safer: direct rollover vs transfer?

Both direct rollovers and direct transfers are generally safe when used correctly:

- In a transfer, you’re staying within IRAs.

- In a direct rollover, you’re moving from an employer plan to an IRA.

The real risk comes with indirect rollovers, where the funds come to you first and the 60-day rule kicks in.

Disclaimer

The information provided in this article is for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial, tax, or legal advice. Retirement account rules especially those involving rollovers, transfers, TSP distributions, and federal employee benefits are highly individualized and may vary based on your personal circumstances, employment history, account type, and current IRS regulations.

Federal Pension Advisors does not guarantee the accuracy or completeness of the information contained herein and is not responsible for errors, omissions, or outdated guidance. Always consult with a qualified financial advisor, tax professional, or attorney before making any decisions related to retirement accounts, rollovers, transfers, or investment strategies.

By reading this material, you acknowledge that no professional relationship has been established and that your financial decisions remain your sole responsibility.

Content References

The information in this article is informed by publicly available guidance from:

- IRS.gov – Publication 590-A & 590-B

Guidelines on IRA transfers, rollovers, 60-day rules, withholding, and reporting requirements. - IRS Topic No. 558 – Retirement Plan Rollovers

Definitions and rules for direct and indirect rollovers. - Thrift Savings Plan (TSP.gov)

Rules for TSP distributions, direct rollovers, in-service withdrawals, and separation requirements. - Internal Revenue Code Sections 408 & 402

Tax treatment and rollover rules for IRAs and qualified retirement plans. - Entrust Group – IRA Transfer vs Rollover Guide

Definitions, examples, and IRA transfer/rollover mechanics. - Kitces.com – IRA Rollover & Transfer Technical Analysis

Detailed walkthroughs on tax reporting, one-per-year rule, and 60-day rollover rules. - FINRA & DOL (Department of Labor)

General guidance around moving retirement accounts and rollover suitability.

Get Updated

Subscribe to our weekly updates for the latest on retirement planning, federal benefits, exclusive webinars, and more!

Download Federal Retirement: Step-by-step Checklist

This comprehensive guide will help you understand your federal benefits, optimize your savings, and plan for a comfortable future.