.png)

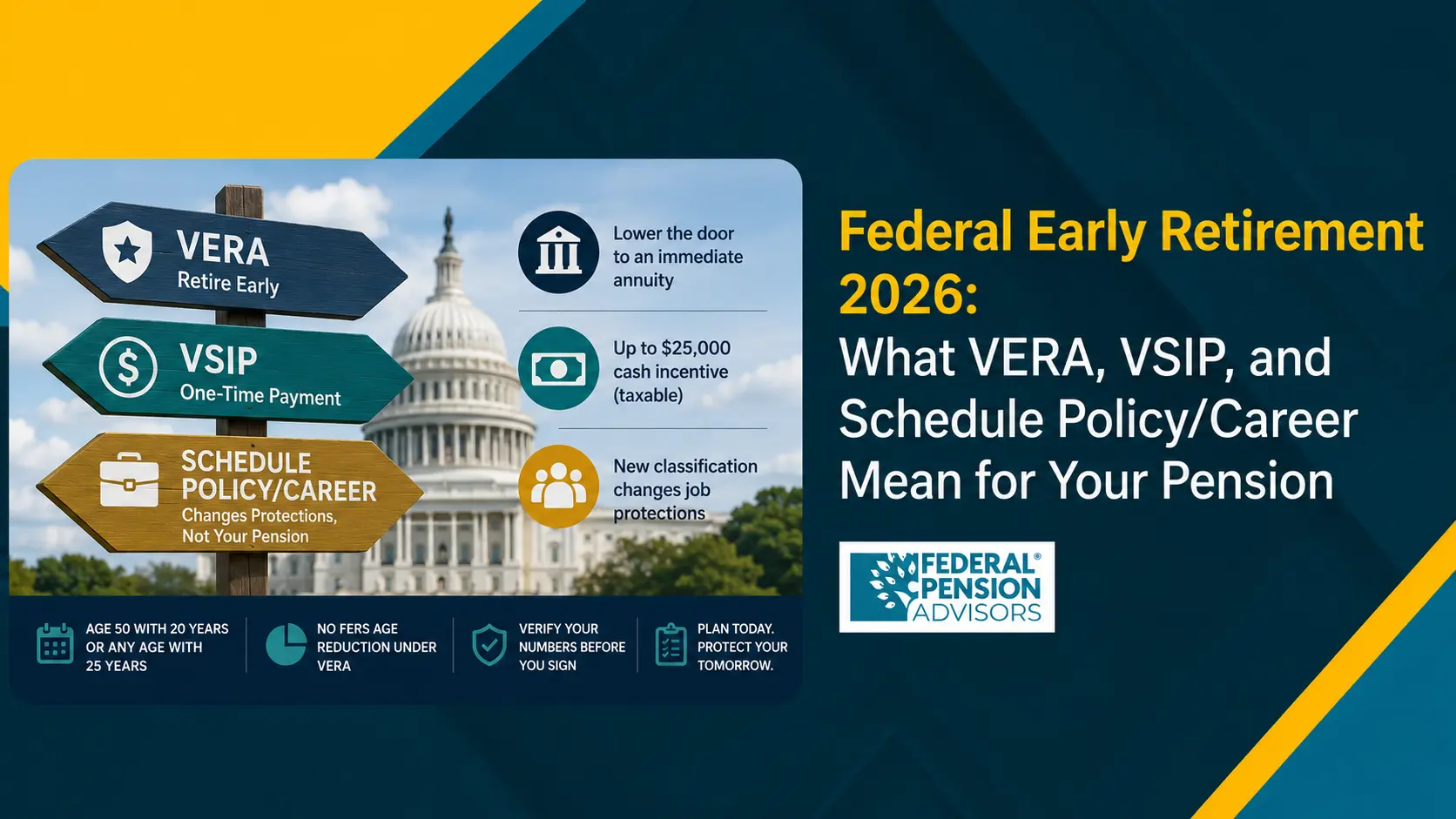

Federal Early Retirement 2026: What VERA, VSIP, and Schedule Policy/Career Mean for Your Pension

Federal early retirement in 2026 means leaving federal service before standard age and service thresholds using two tools: VERA, the Voluntary Early Retirement Authority, and VSIP, the Voluntary Separation Incentive Payment. Under VERA, an eligible employee can retire at age 50 with 20 years of creditable service, or at any age with 25 years, and receive an immediate annuity. FERS employees face no age-based reduction under VERA. CSRS employees under age 55 may still face one.

This year, a third factor sits alongside them. Schedule Policy/Career is a new federal employment classification that changes job protections but does not appear to change the pension you've already earned.

This guide explains how each one works, how an early out affects your FERS or CSRS annuity, and what to verify before you sign anything. If you're weighing an offer, the stakes are high enough that you should treat the decision as a financial planning event, not a personnel one.

What Federal Early Retirement Means in 2026

Federal early retirement in 2026 is the ability to separate from federal service ahead of normal eligibility while still drawing an immediate annuity. It becomes possible when your agency receives early-out authority from OPM, the U.S. Office of Personnel Management.

Why does it exist? Agencies going through restructuring, reorganization, or downsizing can request authority to encourage voluntary departures rather than forcing involuntary cuts.

Two distinct programs drive it. VERA lowers the age and service bar so eligible employees can retire early with an immediate annuity. For FERS employees, VERA avoids the age-based early retirement reduction. CSRS employees under age 55 may still see a reduction.

VSIP is a one-time cash incentive, often offered alongside VERA, to encourage you to take the offer. Neither is an entitlement. Your agency must hold active authority, and your specific position must be covered.

VERA: Voluntary Early Retirement Authority

VERA, the Voluntary Early Retirement Authority, is an OPM-approved tool that temporarily lowers the age and service requirements so eligible employees can retire early with an immediate annuity. Under 5 U.S.C. § 8414(b)(1), you qualify if you're at least age 50 with 20 or more years of creditable service, or you have 25 or more years of service at any age.

According to OPM's Guide to Voluntary Early Retirement Regulations, OPM has no authority to waive either the minimum age or service requirement for VERA eligibility.

Meeting the age-and-service test is necessary but not sufficient. According to OPM, you must also have been continuously employed by your agency for at least 31 days before the agency requested VERA approval, hold a position that is not a time-limited appointment, be free of a final removal decision for misconduct or unacceptable performance, hold a position covered by your agency's plan, and separate before the early-out window closes.

Here's a critical point that surprises many employees. VERA eligibility depends on your agency's specific offer, not OPM's general rule alone. According to Fed Pilot's 2026 VERA guide, your agency decides which positions, components, or geographic locations are covered, so you should always get the specifics in writing from your HR office.

How VERA affects your FERS or CSRS pension

VERA doesn't change the pension formula. According to Fed Pilot, you still receive your High-3 average salary multiplied by your years of service multiplied by 1%, or 1.1% if you retire at age 62 or older with 20 or more years of service. Your High-3 average salary is the average of your highest three consecutive years of base pay.

The difference between the two retirement systems matters here. For FERS, the Federal Employees Retirement System, there's no age-based annuity reduction for retiring early under VERA. For CSRS, the Civil Service Retirement System, employees under age 55 face a reduction.

How much? According to FederalRetirement.net, a CSRS employee under age 55 sees the annuity reduced by 1/6 of 1% per full month under age 55. That works out to 2% per year.

There's also the FERS Special Retirement Supplement, often called the SRS or annuity supplement, which bridges income to Social Security age. According to The Fed Corner, if you retire under a VERA you won't begin receiving the FERS Special Retirement Supplement until you reach your Minimum Retirement Age (MRA), the earliest age a FERS employee can retire with an immediate annuity, which falls between 55 and 57 depending on your birth year.

The supplement then continues until age 62 and is subject to an annual earnings test.

VSIP: Voluntary Separation Incentive Payment

VSIP, the Voluntary Separation Incentive Payment, is a one-time, fully taxable cash buyout offered to encourage voluntary separation. It can accompany VERA or stand alone. The agency must submit a VSIP plan to OPM for approval before offering it.

The amount is capped. According to FederalRetirement.net, the VSIP payment is the lesser of $25,000 or an amount equal to the severance pay the employee would be entitled to, and it's fully taxable as ordinary income in the year received.

One condition gets overlooked often: the repayment trap. According to the same source, if you accept a VSIP and are then re-employed by the federal government within 5 years, including certain federal contract or personal-services roles depending on the reemployment arrangement, you must repay the full VSIP amount before re-employment can begin.

That repayment rule becomes one of the biggest regret drivers for employees who take a buyout and later return to federal work. Treat the $25,000 as money you keep only if you stay out of federal service for five full years.

VERA vs. VSIP: A Side-by-Side Comparison

These two programs are easy to confuse because agencies usually offer them together. They aren't the same thing, and they affect your finances differently.

Sources: OPM Voluntary Early Retirement Authority guidance; FederalRetirement.

Schedule Policy/Career: What It Does to Your Pension

Schedule Policy/Career is a federal employment classification OPM finalized in early 2026 that converts certain policy-influencing career positions into a category with reduced job protections. It's the revived and renamed version of the earlier Schedule F proposal.

According to OPM, the final Schedule Policy/Career rule was issued in February 2026, with implementation actions continuing through the year. The rule applies to positions, not individuals.

The scope has shifted. According to NPR, OPM's earlier rule discussed a potential scope of roughly 50,000 policy-influencing positions. A June 2026 executive order reportedly moved about 8,000 positions into Schedule Policy/Career initially, with the administration not ruling out expanding the pool later.

What changes is workplace protection, not retirement money. According to the Partnership for Public Service, employees reclassified under Schedule Policy/Career would lose certain due process rights, such as advance notice of removal, and in most cases lose the right to appeal their reclassification to the Merit Systems Protection Board. According to Federal News Network, reporting indicates converted employees may face reduced independent appeal or complaint options, including changes to how certain prohibited personnel practice complaints are handled.

Here's the part that matters most for your money: reclassification does not appear to change your earned pension. According to the Federal Employee Benefits Advocates, per OPM, moving into this schedule does not appear to change earned federal retirement benefits. Your retirement annuity and insurance benefits remain intact.

In practical terms, reclassification does not appear to change the FERS or CSRS pension formula, accrued service credit, or earned annuity rights. Verify your individual status with HR or OPM.

There's also no automatic link from reclassification to an early-out offer. Schedule Policy/Career reclassification doesn't automatically create VERA or VSIP eligibility. Early-out offers still depend on separate agency authority and OPM approval. According to the Federal Employee Benefits Advocates, OPM also prohibits agencies from using reclassification as a backdoor substitute for standard Reduction in Force procedures.

Why do employees connect the two? Timing, not regulation. If you sit in a policy-influencing role and your protections are weakening, a VERA/VSIP window may look like a chance to leave on your own terms with your annuity locked in. That can be a sound strategy, but it's a personal financial decision, not a forced consequence of reclassification.

How to Evaluate an Early-Out Offer Before You Sign

Treat any VERA or VSIP offer as a planning problem with a deadline. Run these checks in order.

- Get a written annuity estimate from your HR office. Confirm your exact High-3, creditable service, and any CSRS-component reduction before you decide anything.

- Verify your FEHB continuation. To carry the Federal Employees Health Benefits Program into retirement, you generally need five years of enrollment, though VERA/VSIP windows can trigger a waiver. According to FederalRetirement, OPM may grant pre-approved waivers for employees covered continuously since the beginning of the agency's VSIP/VERA period who retire during that period. Confirm whether the waiver applies to your case with HR.

- Map the SRS timing gap. If you're under your MRA, model the income gap until the supplement begins.

- Model the five-year VSIP repayment risk against any plan to return to federal or contract work.

- Confirm the window dates in writing. You must separate before the early-out period closes.

This is the kind of multi-variable decision where Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, helps clients run the numbers across FERS, CSRS, TSP, and FEHB before committing to an irreversible separation. A single misread on the SRS gap or the VSIP repayment rule can cost far more than the buyout is worth.

The Bottom Line

Federal early retirement in 2026 hinges on three moving parts that are easy to conflate. VERA lowers the door to an immediate annuity. VSIP adds a taxable cash incentive with a five-year repayment string attached. Schedule Policy/Career reshapes job protections without appearing to change the pension you've already earned.

The figures that govern your decision are specific to you: your High-3, your MRA, your SRS timing, and your FEHB eligibility. Verify each one against an official annuity estimate before you act.

Facing an offer with a closing window? A prudent next step is to model the full picture before you sign. Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, works with federal employees to map exactly how a VERA or VSIP offer interacts with their FERS or CSRS annuity, TSP, and health coverage. Schedule a federal retirement review to see what an early-out offer would mean for your specific numbers before the window closes.

Frequently Asked Questions

1. What is the age requirement for federal early retirement under VERA?

Under VERA, you can retire early if you're at least age 50 with 20 years of creditable federal service, or any age with 25 years of service. OPM can't waive these thresholds. Your agency must also hold active VERA authority and cover your specific position for you to qualify.

2. Does early retirement reduce my FERS pension?

No. Under VERA, FERS employees face no age-based annuity reduction. The standard formula still applies: your High-3 average salary multiplied by your years of service multiplied by 1%, or 1.1% if you retire at age 62 or older with at least 20 years of service. CSRS employees under age 55 do face a reduction.

3. How much is a VSIP buyout worth?

A VSIP, or Voluntary Separation Incentive Payment, is capped at the lesser of $25,000 or your calculated severance entitlement. It's fully taxable as ordinary income in the year you receive it. If you return to federal service within five years, including certain federal contract roles, you may have to repay the full amount first.

4. Does Schedule Policy/Career affect my pension?

Based on OPM guidance, reclassification into Schedule Policy/Career does not appear to change your FERS or CSRS pension formula, accrued service credit, or earned annuity rights. The classification changes job protections and appeal rights, not your retirement money. Verify your individual status with HR or OPM before making any decision.

5. Can I take VERA and VSIP at the same time?

Yes. VERA and VSIP are separate programs but agencies frequently offer them together to encourage voluntary departures. VERA provides the early-out authority and immediate annuity, while VSIP provides the one-time cash incentive. Each requires separate OPM approval of the agency's plan, and your position must be covered by both.

6. What happens to my health insurance if I retire early?

To continue FEHB coverage into retirement, you generally need five years of enrollment before separating. During an active VERA or VSIP window, OPM may grant a waiver of that requirement for employees covered continuously since the start of the agency's authority period. Confirm your specific status with your HR office in writing.

Disclaimer

This article is for educational purposes only and does not constitute financial, legal, tax, or retirement advice. Federal retirement benefits vary by individual service history, agency status, and current OPM rules. Verify all benefit figures and eligibility details with OPM.gov, TSP.gov, SSA.gov, and your agency HR office before making any retirement or separation decision.

Get Updated

Subscribe to our weekly updates for the latest on retirement planning, federal benefits, exclusive webinars, and more!

Thomas A. Doherty

Thomas A. Doherty is a retirement planning consultant with 35 years of experience helping federal employees understand complex retirement decisions and benefit programs. His expertise includes federal benefits, pension planning, retirement income strategies, and tax-efficient retirement planning, with a focus on helping clients evaluate early retirement opportunities, buyout offers, and long-term financial outcomes with greater clarity and confidence.

Download Federal Retirement: Step-by-step Checklist

This comprehensive guide will help you understand your federal benefits, optimize your savings, and plan for a comfortable future.