.png)

How to Open an IUL Account: Steps, Costs, Risks, and Questions to Ask

To open an IUL account, you apply for an indexed universal life (IUL) insurance policy through a licensed life insurance agent or carrier, complete underwriting, review the policy illustration, and pay your first premium to activate coverage. Underwriting usually includes a medical exam. There's no standalone IUL account you open at a bank or brokerage.

As Insurance Geek explains, an IUL is a contract between you and a life insurance company, not a deposit account. This guide walks through every step, the real costs, the risks federal employees should weigh, and the exact questions to ask before you sign.

Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, often fields questions about IUL from federal workers who already hold strong government retirement benefits. Before you treat an IUL as a retirement vehicle, it helps to understand how it fits, or doesn't fit, alongside the Federal Employees Retirement System (FERS) and the Thrift Savings Plan (TSP), the federal government's tax-advantaged retirement savings program.

What Is an IUL Account?

An indexed universal life (IUL) policy is a form of permanent life insurance. It combines a death benefit with a cash value component whose growth is tied to a market index, most commonly the S&P 500.

Your money is not invested directly in the market. Instead, insurers generally credit interest using an index-linked formula, often supported by hedging strategies. That crediting is subject to a cap and a floor.

The cash value grows tax-deferred, and you can access it later through loans or withdrawals. Because the policy carries both insurance charges and indexing limits, it behaves very differently from a brokerage account or an index fund. That's why you should review the policy illustration and contract language carefully.

How to Open an IUL Account: Step by Step

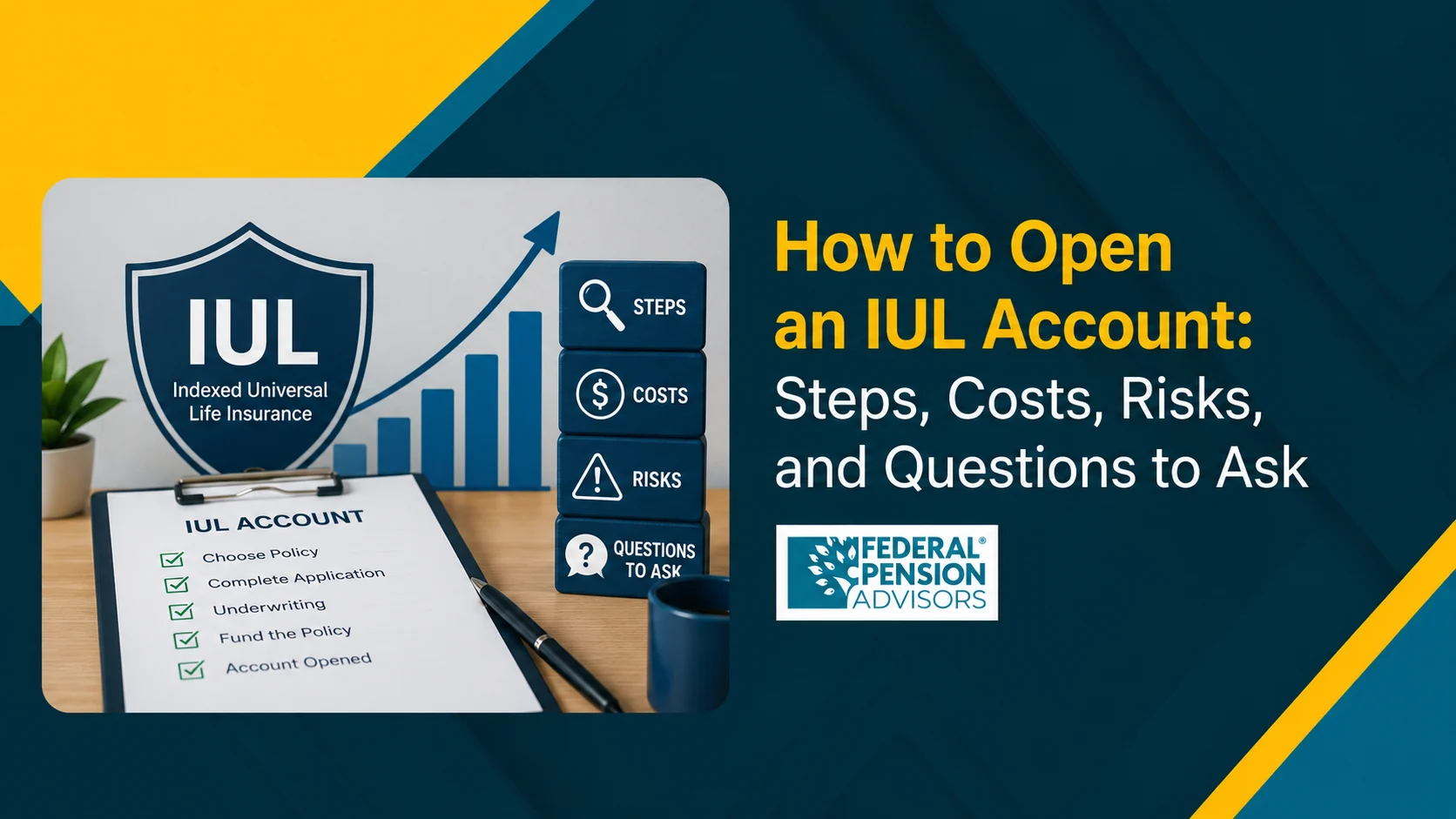

Opening an IUL involves six sequential steps: assess your needs, compare carriers, complete an application, undergo underwriting, review the illustration, and fund the policy. Here is each step in order.

- Assess your financial goals. Decide whether you primarily need a death benefit, tax-deferred cash value growth, or both. SmartAsset advises evaluating your overall financial situation first, because the product only makes sense for specific goals.

- Compare carriers and policy structures. Different insurers offer different caps, participation rates, and fee schedules. An independent agent who can show you multiple carriers, rather than a single company's brochure, helps you compare honestly.

- Complete the application. You'll disclose health, lifestyle, and financial information. Capital for Life notes that this stage establishes your eligibility and premium rate.

- Undergo underwriting. Underwriting may include a medical exam, a health questionnaire, lab work, a prescription history review, or accelerated underwriting, depending on the carrier and applicant. Insurance Geek notes that lab work from the past 12 months can sometimes replace a new exam and shave one to two weeks off the process.

- Review the policy illustration. Once approved, the carrier issues an illustration, the single most important document in the process, according to Insurance Geek. It projects how your cash value could grow under stated assumptions.

- Fund the policy. Pay your first premium to activate coverage. Then monitor the policy annually and adjust as your circumstances change.

How Much Does an IUL Account Cost?

Internal charges plus the growth limits that cap your returns drive the cost of an IUL. Unlike a low-cost index fund, an IUL deducts several layers of fees from your cash value every year, and those fees rise as you age.

The main charges include the cost of insurance (COI), which covers the death benefit and increases with the insured's age, premium expense charges, and administrative fees. Surrender charges can be significant in the early years and usually decline over time. The exact schedule depends on the policy contract.

On the growth side, FIG Marketing explains that a participation rate of 80% credits only 80% of an index gain, a cap rate limits the maximum credited return, and a spread fee subtracts a fixed percentage from the index return.

These growth limits matter as much as the fees. Some IUL strategies may use caps in the high single digits or low double digits, but caps vary by carrier and can change over time. If a cap applies and the S&P 500 rises above it, the policy credits only up to the cap.

The 0% floor protects you from market losses. But as Insurance & Estates points out, that floor isn't truly free. In a flat year, insurance and administrative charges still come straight out of your cash value.

IUL vs. TSP: a federal employee comparison

Most federal employees already have access to the TSP, so the most useful comparison is between an IUL and the TSP, not between an IUL and a generic investment account. The key difference is purpose. The TSP is a low-cost retirement savings plan, while an IUL is a life insurance contract that also builds cash value.

Have you captured the full FERS agency match yet? For most federal employees who haven't, financial commentators broadly agree that maxing the TSP first is the higher-priority move. The match is an immediate employer contribution that's difficult for an insurance product to offset.

According to TSP.gov, the 2026 elective deferral limit is $24,500. It rises to $32,500 for those age 50 and older with the standard catch-up, and up to $35,750 for participants ages 60 to 63 under the SECURE 2.0 enhanced catch-up.

What Are the Risks of an IUL Account?

The primary risks of an IUL are high internal costs, capped growth, surrender charges, lapse risk from underfunding, and the gap between illustrated and actual returns. These risks are significant enough that regulators have taken notice.

The Financial Industry Regulatory Authority (FINRA), the self-regulatory body overseeing U.S. broker-dealers, identifies indexed universal life as a type of universal life insurance tied to a stock index rather than to investments the policyholder selects. You should review policy costs, surrender charges, and non-guaranteed assumptions carefully before buying. That guidance matters if you're a federal employee nearing retirement who may be approached as an IUL prospect.

Several specific risks deserve attention:

- Capped growth limits your upside. As Insurance & Estates notes, you give up some market upside in exchange for downside protection. Your cash value typically grows more like a moderate bond portfolio than a stock portfolio, despite the S&P 500 linkage.

- Illustrations are projections, not promises. Wealthvieu cautions that a policy illustration showing 7% to 8% hypothetical returns is a best-case scenario under current caps, which the insurer can later change.

- Surrender charges lock you in. Cancelling early can be costly, because surrender charges are significant in the early years. The exact schedule varies by contract.

- Underfunding can cause a lapse. Western & Southern notes that insufficient premiums can cause the policy to lapse, potentially triggering tax consequences and loss of coverage.

- Loan and tax pitfalls exist. Western & Southern warns that a policy classified as a modified endowment contract can make distributions taxable, with a possible 10% additional tax before age 59½.

Questions to Ask Before You Open an IUL Account

The right questions before signing help protect you from misunderstanding non-guaranteed assumptions, policy charges, and long-term funding requirements. Bring this list to any IUL consultation.

- What is the current cap rate, participation rate, and spread, and can the insurer change them after I buy?

- What does the illustration look like at a conservative 4% to 5% growth rate, not just the best-case projection? (Wealthvieu specifically recommends requesting a lower-rate illustration.)

- What happens to my cash value if the index returns 0% for several years in a row?

- What is the full surrender charge schedule, year by year?

- How will the cost of insurance rise as I age, especially after 70?

- How much must I pay each year to keep the policy in force and avoid a lapse?

- How does this compare to maxing my TSP and FERS benefits first?

IUL and Your Federal Benefits

Evaluate an IUL only after securing your core federal benefits. The TSP offers a FERS agency match worth up to 5% of pay, an immediate, guaranteed return that no IUL can replicate, and its funds are generally low-cost compared with many retirement investment options.

OPM, the U.S. Office of Personnel Management, administers the broader federal benefits framework, including the Federal Employees Health Benefits (FEHB) program. FEHB can be one of the most valuable federal retirement benefits for eligible employees, so review it before committing cash flow to a private insurance strategy.

Federal Pension Advisors generally encourages federal workers to fully fund the TSP, capture the FERS match, and understand their FEHB and CSRS (Civil Service Retirement System) or FERS annuity projections before committing premium dollars to a permanent life insurance product.

Some high earners who need permanent life insurance and have already addressed core retirement savings may consider an IUL. But suitability depends on the policy design, funding ability, tax situation, and insurance need. It should complement, never replace, the federal benefits you've already earned.

The Bottom Line

Opening an IUL account means applying for an indexed universal life insurance policy, passing underwriting, reviewing the illustration carefully, and funding the policy. It doesn't mean opening an account at a bank.

The product offers tax-deferred cash value growth with downside protection, but it carries internal costs, capped returns, and surrender charges that FINRA encourages you to review closely before buying. For federal employees, the smarter sequence is usually to max the TSP and FERS match and confirm your FEHB and annuity plans before considering an IUL.

To review whether an IUL fits alongside your federal benefits, connect with Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, for guidance tailored to your FERS or CSRS situation.

Frequently Asked Questions

1. How do I open an IUL account?

You open an IUL by applying for an indexed universal life policy through a licensed agent or carrier, completing underwriting, reviewing the policy illustration, and paying your first premium. Underwriting may include a medical exam or accelerated review. There's no separate bank account. An IUL is a life insurance contract.

2. How much does an IUL cost?

An IUL's cost includes the cost of insurance, administrative fees, premium charges, and surrender charges. Surrender charges can be significant in the early years and usually decline over time, though the exact schedule depends on the policy. The cost of insurance also rises as you age, which can erode cash value if the policy is underfunded.

3. Is an IUL a good investment for federal employees?

For most federal employees, maxing the TSP and capturing the FERS agency match of up to 5% comes first, because that match is a guaranteed return. Some high earners who need permanent life insurance and have addressed core savings may consider an IUL. But it's insurance with capped growth, not a substitute for the TSP.

4. What is the difference between an IUL and the TSP?

The TSP, or Thrift Savings Plan, is a low-cost federal retirement savings plan with uncapped market exposure and an agency match. An IUL is a life insurance contract with a death benefit and capped, index-linked cash value. The TSP is built for retirement savings. The IUL is built around insurance.

5. Can I lose money in an IUL?

Your indexed cash value won't drop due to market losses, because of the 0% floor. But as Insurance & Estates notes, insurance and administrative fees are still deducted in flat years, so your cash value can decline. Surrendering early can also cost a significant share of your cash value.

6. What are the risks of an IUL account?

The main risks are high internal fees, capped growth that limits upside, steep surrender charges, lapse risk from underfunding, and illustrations that overstate likely returns. FINRA identifies indexed universal life as a type of universal life tied to a stock index, and advises reviewing costs, surrender charges, and non-guaranteed assumptions before buying.

Disclaimer

This article is for educational purposes only and does not constitute financial, tax, insurance, or retirement planning advice. Indexed universal life policies involve fees, policy charges, surrender charges, and non-guaranteed assumptions. Federal employees should verify current benefit rules through OPM.gov, TSP.gov, and IRS.gov, and consult a licensed professional before making decisions.

Get Updated

Subscribe to our weekly updates for the latest on retirement planning, federal benefits, exclusive webinars, and more!

Michael A. Fox

Michael A. Fox is a seasoned Financial Advisor and Retirement Income Planning Specialist with more than 25 years of experience helping individuals and families make informed retirement decisions. His focus is on retirement income planning, protection strategies, and helping clients build long-term financial confidence through clear, practical guidance.

Download Federal Retirement: Step-by-step Checklist

This comprehensive guide will help you understand your federal benefits, optimize your savings, and plan for a comfortable future.