.png)

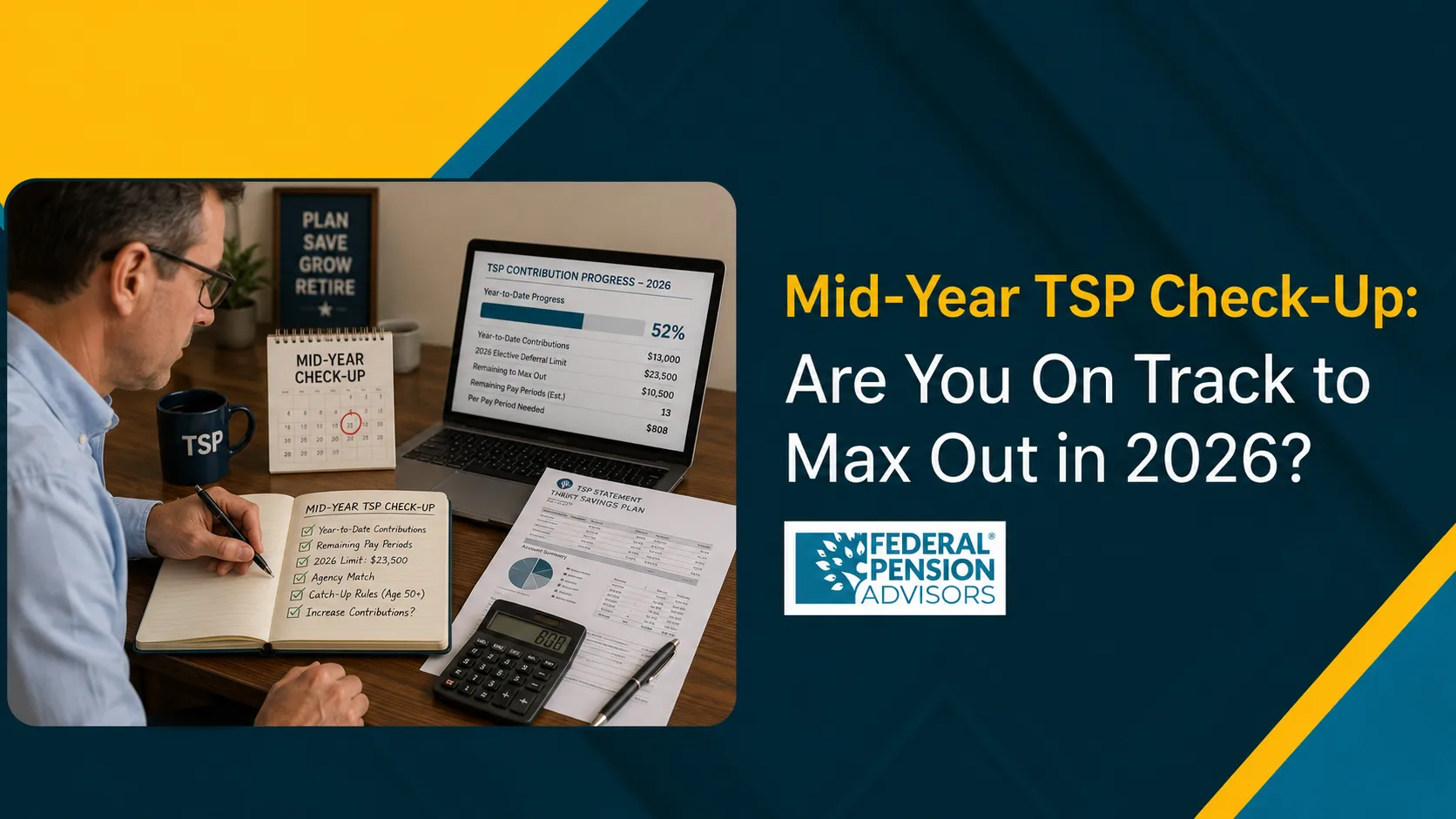

Mid-Year TSP Check-Up: Are You On Track to Max Out in 2026?

A mid-year TSP check-up is a contribution review you run around June or July to confirm your year-to-date Thrift Savings Plan (TSP) deposits are on pace to hit your 2026 target by the final pay period. Half the year's pay periods are now behind you. This is the moment to compare what you've actually contributed against what you'd need to contribute to max out, and to correct course while there's still time.

This guide from Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, walks you through the figures, the math, and the adjustments that keep your plan on track.

The TSP is the federal government's tax-advantaged retirement savings program, comparable to a private-sector 401(k). If you're under the Federal Employees Retirement System (FERS), the system covering most federal workers hired since 1984, the TSP is one of three legs of your retirement income. The other two are the FERS basic annuity and Social Security.

Getting your mid-year TSP check-up right at the halfway mark keeps the savings portion of your federal retirement plan on track.

Why a Mid-Year TSP Check-Up Matters

The payroll system generally stops your employee contributions once the annual limit is reached. Front-loading too aggressively can cause you to miss agency matching contributions in later pay periods.

TSP guidance is clear: contributions that would exceed the IRS elective deferral limit are not accepted, and for employees under 50, contributions generally stop once the cap is reached. That automatic stop is the hidden trap of maxing out.

Here's why timing is everything. The TSP agency match is calculated per pay period, not annually. Contribute so much early in the year that you hit $24,500 in October, and your contributions stop, along with the agency match for November and December.

A check-up in June can help catch a too-aggressive pace before it affects later matching contributions.

The opposite problem is just as common. Many federal employees set a flat percentage in January, never revisit it, and reach December short of the limit with no way to recover the unused tax-advantaged space. Your mid-year review is one of the most practical chances to find and fix both errors, with enough time to make a realistic adjustment before year-end.

The 2026 TSP Contribution Limits You Need to Know

The TSP contribution limit 2026 for regular employee elective deferrals is $24,500, up from $23,500 in 2025. This limit applies to the combined total of your Traditional TSP (tax-deferred) and Roth (after-tax) contributions, and it does not include agency matching contributions. The increase reflects the IRS cost-of-living adjustment for the 2026 plan year.

If you're age 50 or older at any point during 2026, you can contribute additional catch-up contributions. The 2026 catch-up limit is $8,000, which brings your combined elective deferral and catch-up limit to $32,500.

A higher super catch-up applies to a specific age band. Under Section 109 of the SECURE Act 2.0, employees who turn 60, 61, 62, or 63 during 2026 have a catch-up limit of $11,250, for a combined limit of $35,750. In the year you turn 64, the catch-up limit drops back to $8,000.

One important 2026 change affects higher earners. Eligible TSP catch-up contributions must be made as Roth TSP contributions if your TSP-eligible wages exceeded $150,000 in 2025. If this applies to you, the TSP automatically converts your catch-up dollars to Roth once you reach the elective deferral limit, so you don't need to do anything manually. This wage threshold may be adjusted in future years.

2026 TSP contribution limits at a glance

Source: Thrift Savings Plan (tsp.gov), 2026 contribution limits.

How to Run Your Mid-Year TSP Check-Up in Four Steps

Your mid-year TSP check-up takes four steps. Pull your year-to-date total, identify your target, count your remaining pay periods, and recalculate your per-period contribution. The whole review takes about 15 minutes once you have your latest Leave and Earnings Statement (LES) in hand.

Step 1: Pull your year-to-date contributions. Log in to your account at tsp.gov or check the TSP year-to-date figure on your most recent LES. Record the exact dollar amount you've contributed in employee elective deferrals so far in 2026. Don't include the agency match, because the limit applies only to your own contributions.

Step 2: Identify your 2026 target. For most employees this is the $24,500 elective deferral limit. If you're 50 or older, add your catch-up amount to reach $32,500 or $35,750, depending on your age band.

Step 3: Count your remaining pay periods. Most federal employees have 26 pay periods in 2026, but confirm your agency's payroll calendar. By mid-year, many employees have roughly 13 pay periods left, and the exact number drives the math.

Step 4: Recalculate your per-period amount. Subtract your year-to-date total from your target, then divide by the remaining pay periods. That figure is what you contribute each remaining pay period. Adjust your election through your agency payroll system or Form TSP-1, if your agency still uses the form, when it differs from your current setting.

A Worked Example: The On-Track Calculation

The clearest way to see the math is with a real planning scenario. Take a FERS employee, age 45, aiming for the full $24,500 in 2026. To spread the TSP contribution amount evenly across all 26 pay periods, the per-period target is $943, which is the figure you reach by dividing $24,500 by 26, according to figures published by the Interior Business Center.

Now suppose this employee runs a check-up at the end of June and finds they've contributed only $5,200 year-to-date. That's well behind the roughly $12,259 they should have reached at the halfway point.

With 13 pay periods left, the corrected math is straightforward. Subtract $5,200 from $24,500 to get $19,300 remaining. Divide that by 13 pay periods, and you land at about $1,485 per pay period for the rest of the year.

That's a large jump, and it shows why the check-up matters. Caught in June, the employee has room to redistribute. Caught in November, the same shortfall would be impossible to close.

The lesson is simple. The earlier you check, the gentler the correction.

On-track vs. behind: a mid-year comparison

Illustrative scenario. Per-period base figure ($943) sourced from the Interior Business Center; remaining figures calculated from the 2026 TSP elective deferral limit.

Don't Sacrifice the Agency Match While Maxing Out

The most expensive mid-year mistake is front-loading contributions so heavily that you hit the limit early and forfeit agency matching contributions in the final pay periods. If you stop your employee contributions, your agency matching contributions also stop, because matching is calculated on the first 5% of basic pay you contribute each pay period.

For FERS employees, the stakes are concrete. The first 3% of pay you contribute is matched dollar-for-dollar, and the next 2% is matched at 50 cents on the dollar. Contributing at least 5% of your basic pay each pay period earns an agency match equal to 4% of pay, which together with the Agency Automatic (1%) Contribution totals 5%.

Reach the annual limit early and stop contributing in November, and you forgo that TSP agency match for every remaining pay period.

The fix is to aim for a steady per-period contribution that spreads your target evenly across all 26 pay periods. Your mid-year check-up is precisely where you verify your pace is even, not front-loaded. If your June review shows you're on track to hit $24,500 before the final pay period, lower your election slightly so your last contribution lands in pay period 26.

What to Do If You're Behind, Ahead, or Right on Track

Behind pace? Increase your per-period election immediately through your agency payroll system or Form TSP-1, and consider whether a temporary larger contribution for one or two pay periods can close part of the gap. The sooner you adjust, the smaller the per-period increase needs to be.

Ahead of pace? Confirm you won't hit the limit before the final pay period. Reaching the cap early can stop your employee contributions before year-end and forfeits the remaining agency match. Reduce your election so contributions continue through pay period 26.

Right on track? Your job is to verify and document. Confirm your per-period amount still divides cleanly into your remaining target, note any pay raise or step increase that changes your percentage-based contribution, and set a calendar reminder for an October re-check.

A consultation with Federal Pension Advisors can help review whether your contribution pace, catch-up eligibility, Roth versus Traditional TSP split, and broader FERS retirement plan are aligned.

The Bottom Line

A mid-year TSP check-up is the difference between hoping you'll max out and knowing you will. Pull your year-to-date total, compare it to the $24,500 elective deferral limit, and recalculate your per-period contribution across your remaining pay periods. You catch both the front-loading trap that forfeits the agency match and the slow-pace shortfall that leaves tax-advantaged space on the table.

Federal Pension Advisors helps federal employees integrate their TSP strategy with their full FERS retirement plan. Schedule a mid-year review to confirm you're on track for 2026 and to build the contribution plan that carries into next year.

Frequently Asked Questions

1. What is the maximum you can contribute to TSP in 2026?

The TSP elective deferral limit is $24,500 for employees of any age, according to the Thrift Savings Plan. If you're 50 or older, you can add an $8,000 catch-up contribution for a $32,500 total. Those turning 60 to 63 in 2026 can contribute an $11,250 catch-up, reaching $35,750.

2. How much should I contribute per pay period to max out TSP in 2026?

To reach the $24,500 limit evenly across all 26 pay periods, contribute about $943 per pay period, according to figures from the Interior Business Center. If you start mid-year or fall behind, divide your remaining target by your remaining pay periods to find the corrected per-period amount.

3. What happens if I max out my TSP before the end of the year?

Your employee contributions generally stop once you reach the applicable annual limit, according to the Thrift Savings Plan. For FERS employees this also stops the agency matching contributions in remaining pay periods, since matching is calculated per pay period. You forfeit employer-provided retirement contributions you would otherwise earn.

4. Does the TSP agency match count toward the TSP contribution limit?

No. The $24,500 elective deferral limit applies only to your own employee contributions, according to the Thrift Savings Plan. Agency automatic and matching contributions don't count against it. That's why maxing out your contributions and earning the full 5% FERS match are separate goals.

5. When should I do a mid-year TSP check-up?

Run your mid-year TSP check-up around June or July, when roughly 13 of the year's 26 pay periods remain. This timing lets you compare your year-to-date contributions against your target and correct your per-period amount while there's still enough runway to close any gap comfortably.

6. Can I change my TSP contribution amount in the middle of the year?

Yes. You can adjust your TSP contribution amount at any time by submitting Form TSP-1 to your agency or using your payroll system's electronic election option. The change takes effect in an upcoming pay period, which makes mid-year adjustments the standard tool for staying on pace to max out.

Disclaimer

This article is for informational purposes only and does not constitute financial, tax, or investment advice. TSP contribution limits, catch-up rules, and payroll procedures may vary by individual situation. Verify all figures with TSP.gov, IRS guidance, and your agency payroll office before making contribution changes.

Get Updated

Subscribe to our weekly updates for the latest on retirement planning, federal benefits, exclusive webinars, and more!

Brad Myers

Brad Myers is a Federal Benefits Specialist with 17 years of experience helping federal employees maximize their retirement benefits and make informed financial decisions. As a ChFEBC professional, he specializes in Thrift Savings Plan (TSP) strategies, FERS and CSRS retirement planning, pension maximization, and federal employee benefits, helping clients optimize their retirement savings and long-term financial security.

Download Federal Retirement: Step-by-step Checklist

This comprehensive guide will help you understand your federal benefits, optimize your savings, and plan for a comfortable future.