.png)

TSP Funds Explained: A Beginner's Guide to the 5 Core Funds (2026)

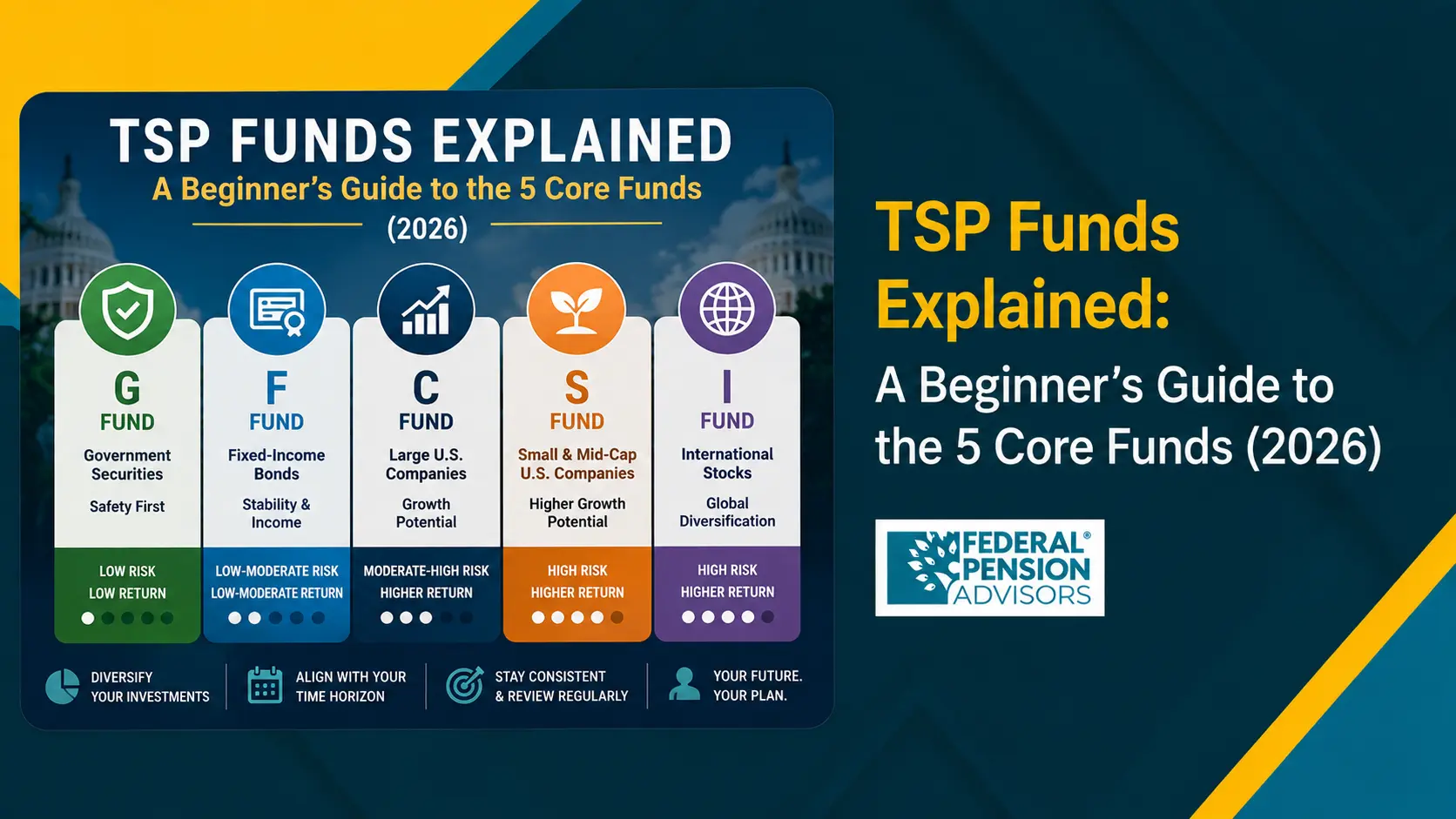

Here are the TSP funds explained simply. The Thrift Savings Plan (TSP) is the federal government's tax-advantaged retirement savings program. It offers five core investment funds: the G Fund (government securities), the F Fund (fixed-income bonds), the C Fund (large U.S. companies), the S Fund (small and mid-sized U.S. companies), and the I Fund (international stocks).

Each fund carries a different mix of risk and growth potential. Your job as a new federal investor is to combine them in a way that matches your age, your timeline, and how much short-term loss you can tolerate.

If you've just started contributing to the TSP, the alphabet soup of fund letters can feel overwhelming. This guide breaks down what each of the 5 TSP funds holds, how they've performed, who each one suits, and how to build a starter allocation.

Key contribution limits and fund details come from official sources such as TSP.gov and IRS.gov. Some performance context comes from reputable financial and federal benefits publications.

What the TSP Is and Why Your Fund Choice Matters

The TSP is the defined-contribution retirement plan for federal employees and members of the uniformed services. It works much like a private-sector 401(k). You contribute a portion of each paycheck, your agency may match part of it, and the money grows tax-advantaged until retirement.

For employees under FERS, the Federal Employees Retirement System, the TSP is one of three retirement income pillars. The other two are the FERS basic annuity and Social Security.

Your fund choice still matters. Even if your contributions land in an age-appropriate L Fund by default, you should check whether that allocation fits your retirement timeline, your risk tolerance, and your broader financial plan.

According to TSP, individual fund expense ratios ran around 0.034% to 0.035% for 2025. That makes them very low-cost compared with many private-sector retirement plan options. Low fees help, but they can't rescue a poorly chosen allocation.

The 5 TSP Funds Explained

Below is a plain-language breakdown of each core fund. The TSP funds are index funds. Each one passively tracks an established market benchmark instead of trying to beat the market through active stock-picking.

The G Fund: government securities

The G Fund, the Government Securities Investment Fund, holds only short-term, nonmarketable U.S. Treasury securities issued specifically to the TSP. It's the one TSP fund that can't lose value. The U.S. government guarantees payment of principal and interest.

According to the TSP, the G Fund returned 4.44% over the one-year period and 2.76% annualized over the 10 years ending December 31, 2025.

The trade-off for that safety is modest growth. Over long horizons, the G Fund may offer limited growth compared with stock funds, so investors with decades until retirement may need more growth exposure. Think of the G Fund as your portfolio's safe harbor. It's valuable for capital preservation as retirement nears and less suited to decades-long growth.

The F Fund: fixed-income bonds

The F Fund, the Fixed Income Index Investment Fund, tracks the Bloomberg U.S. Aggregate Bond Index. That's a broad basket of U.S. government, mortgage-backed, corporate, and foreign bonds. Unlike the G Fund, the F Fund can lose value when interest rates rise, because bond prices and interest rates move in opposite directions.

According to the TSP's official Fund Information sheet, the F Fund returned 2.11% annualized over the 10 years ending December 31, 2025. That's modest next to the stock funds. Its 7.21% one-year return reflected more favorable bond conditions as interest rates declined.

The F Fund adds diversification because bonds often behave differently from stocks. Its long-run returns have been low, so investors typically use it as a stabilizer rather than a growth engine.

The C Fund: large U.S. companies

The C Fund, the Common Stock Index Investment Fund, tracks the Standard & Poor's 500 (S&P 500) Index, roughly 500 of the largest U.S. companies. It's the workhorse equity fund for most federal investors and the largest holding in many TSP accounts.

According to the TSP's official Fund Information sheet, the C Fund returned 17.85% in 2025 and 14.79% annualized over the 10 years ending December 31, 2025. That closely tracks the S&P 500's 14.82% over the same period.

Stocks carry real downside risk, though. According to the Government Executive, the C Fund fell 0.76% in February 2026. According to FedSmith, it dropped roughly 4.4% in the first quarter of 2026 amid market volatility. Over long periods, the C Fund has historically ranked among the strongest-performing core TSP funds, though future returns aren't guaranteed.

The S Fund: small and mid-sized U.S. companies

The S Fund, the Small Capitalization Stock Index Investment Fund, tracks the Dow Jones U.S. Completion Total Stock Market Index. That index covers essentially every publicly traded U.S. company not in the S&P 500. You get small and mid-sized firms, which can grow faster than large companies but also fall harder.

The S Fund swings more than the C Fund. According to FedSmith, the S Fund finished the first quarter of 2026 down about 1.2% after a positive start to the year.

Many investors pair the S Fund with the C Fund to capture the full U.S. stock market. The C Fund broadly covers large U.S. companies, while the S Fund adds exposure to many small and mid-sized U.S. companies outside the S&P 500.

The I Fund: international stocks

The I Fund, the International Stock Index Investment Fund, invests outside the United States. It tracks the MSCI ACWI IMI ex USA ex China ex Hong Kong Index. That gives you exposure to developed and emerging markets across Europe, Asia, the Pacific, and Canada, while excluding China and Hong Kong.

The I Fund can be the most volatile core fund because it carries both stock-market risk and currency risk. It isn't currency-hedged, so a stronger U.S. dollar reduces returns.

According to FedSmith, the I Fund was the standout performer of 2025 with a 32.45% return. It then led the early-2026 reversal, posting the largest single-month loss in March 2026. The I Fund is the classic example of why diversification matters. Leadership among funds can change quickly.

TSP Fund Comparison Table

This TSP fund comparison summarizes the five core funds side by side. The 10-year annualized returns are the fund-level figures (net of fees) reported in the official TSP Fund Information sheet for the period ending December 31, 2025.

The L Funds: A Hands-Off Alternative

If choosing among five funds feels like too much, the TSP offers Lifecycle (L) Funds. Each L Fund holds a professionally designed mix of all five core funds, and that mix automatically grows more conservative as a target retirement date approaches.

You pick the L Fund closest to the year you expect to start withdrawing money. Someone retiring around 2048 to 2052 would pick the L 2050 Fund, for example, and the TSP rebalances for you.

According to Federal News Network reporting, the L 2050 Fund posted a 10-year average annual return of roughly 8.67%. The more conservative L Income Fund, for those already withdrawing, returned roughly 4.38%. (These figures reflect 2025 reporting. Confirm current returns on TSP.gov before publishing.)

The L Funds trade a small amount of long-run growth for simplicity and automatic discipline. That makes them a sensible default for beginners who prefer a set-and-forget approach.

How Much Should a Beginner Contribute?

Before you optimize your fund mix, capture the free money. Under FERS, your agency contributes 1% of your basic pay automatically. It then matches your own contributions dollar-for-dollar on the first 3% and 50 cents on the dollar for the next 2%, up to a 5% agency or service contribution when you contribute at least 5% yourself.

According to the IRS, the 2026 elective deferral limit is $24,500. There's an $8,000 catch-up contribution for participants age 50 and older, and a higher $11,250 catch-up limit for those age 60 to 63 under SECURE 2.0.

Here's a practical beginner rule. Contribute at least 5% of basic pay to receive the full agency or service contribution. That generally includes the 1% automatic contribution plus up to 4% in matching contributions.

Leaving the match on the table is one of the costliest mistakes a new federal employee can make.

Building a Starter Allocation

Treat any sample allocation framework as educational, not a personalized recommendation. There's no single best allocation. The right mix depends on your age, your risk tolerance, and your years until retirement.

As a general framework, younger investors with decades ahead can tolerate more stock exposure in the C, S, and I Funds, because they have time to recover from downturns. Those nearing retirement typically shift toward the G and F Funds to protect what they've accumulated.

A common beginner approach weights heavily toward the C Fund for stability within equities. It adds the S and I Funds for growth and global exposure, then gradually increases the G and F Funds as retirement approaches.

This kind of allocation decision is exactly where personalized federal retirement planning helps. Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, works with federal employees to align TSP allocations with their broader FERS retirement picture rather than treating the account in isolation.

The Bottom Line

The 5 TSP funds give federal employees a low-cost, well-diversified set of building blocks for retirement. The G and F Funds prioritize safety, the C and S Funds capture U.S. stock growth, and the I Fund adds international exposure. The L Funds package all of them together for hands-off investors.

Start by securing the full 5% FERS match. Choose an allocation that fits your age and risk tolerance, then revisit it as you move toward retirement.

TSP figures and contribution limits change every year, so verify any number against TSP.gov and IRS.gov before you act. This article is for educational purposes and is not individualized investment, tax, or legal advice.

To map your fund choices to your full federal retirement picture, Federal Pension Advisors offers planning support built specifically for federal employees.

Frequently Asked Questions

1. What are the 5 TSP funds?

The 5 TSP funds are the G Fund (government securities), the F Fund (fixed-income bonds), the C Fund (large U.S. companies tracking the S&P 500), the S Fund (small and mid-sized U.S. companies), and the I Fund (international stocks). Each carries a different balance of risk and growth potential.

2. Which TSP fund is the safest?

The G Fund is the safest TSP fund. It invests in special U.S. Treasury securities and is the only fund that can't lose value, because the U.S. government guarantees principal and interest. According to the TSP, it returned 4.44% over the one year ending December 31, 2025.

3. Which TSP fund has the highest return?

Historically, the C Fund has delivered among the strongest long-term returns of the core funds, at 14.79% annualized over the 10 years ending December 31, 2025, per the TSP's official Fund Information sheet. In single years, leadership can shift. The I Fund led the core funds in 2025 with a 32.45% return.

4. How much should I contribute to my TSP?

Contribute at least 5% of your basic pay to receive the full agency or service contribution under FERS. For 2026, the IRS elective deferral limit is $24,500, with an extra $8,000 catch-up for those 50 and older. The 5% contribution generally secures the 1% automatic contribution plus up to 4% in matching contributions.

5. What is the difference between the C, S, and I Funds?

The C Fund holds large U.S. companies in the S&P 500. The S Fund holds small and mid-sized U.S. companies not in the S&P 500. The I Fund holds international stocks outside the United States. Together the C and S Funds cover the entire U.S. stock market, while the I Fund adds global diversification.

6. Should a beginner use the L Funds instead of picking funds?

The L Funds suit beginners who prefer a hands-off approach. Each Lifecycle Fund automatically blends all five core funds and grows more conservative as your target retirement date nears. According to Federal News Network reporting, the L 2050 Fund returned roughly 8.67% annualized over 10 years, trading slightly lower growth for built-in rebalancing.

Disclaimer

This article is for educational purposes only and should not be treated as individualized investment, tax, legal, or retirement planning advice. TSP rules, fund returns, contribution limits, and federal benefits guidance can change, so verify current details with TSP.gov, IRS.gov, and your agency before making decisions. Consider speaking with a qualified federal retirement advisor for guidance based on your personal situation.

Get Updated

Subscribe to our weekly updates for the latest on retirement planning, federal benefits, exclusive webinars, and more!

Brad Myers

Brad Myers is a Federal Benefits Specialist with 17 years of experience helping federal employees maximize their retirement benefits and make informed financial decisions. As a ChFEBC professional, he specializes in Thrift Savings Plan (TSP) strategies, FERS and CSRS retirement planning, pension maximization, and federal employee benefits. Brad has helped more than 1,000 federal employees better understand their retirement options and build strategies designed to support long-term financial security.

Download Federal Retirement: Step-by-step Checklist

This comprehensive guide will help you understand your federal benefits, optimize your savings, and plan for a comfortable future.

Recent Post's