.png)

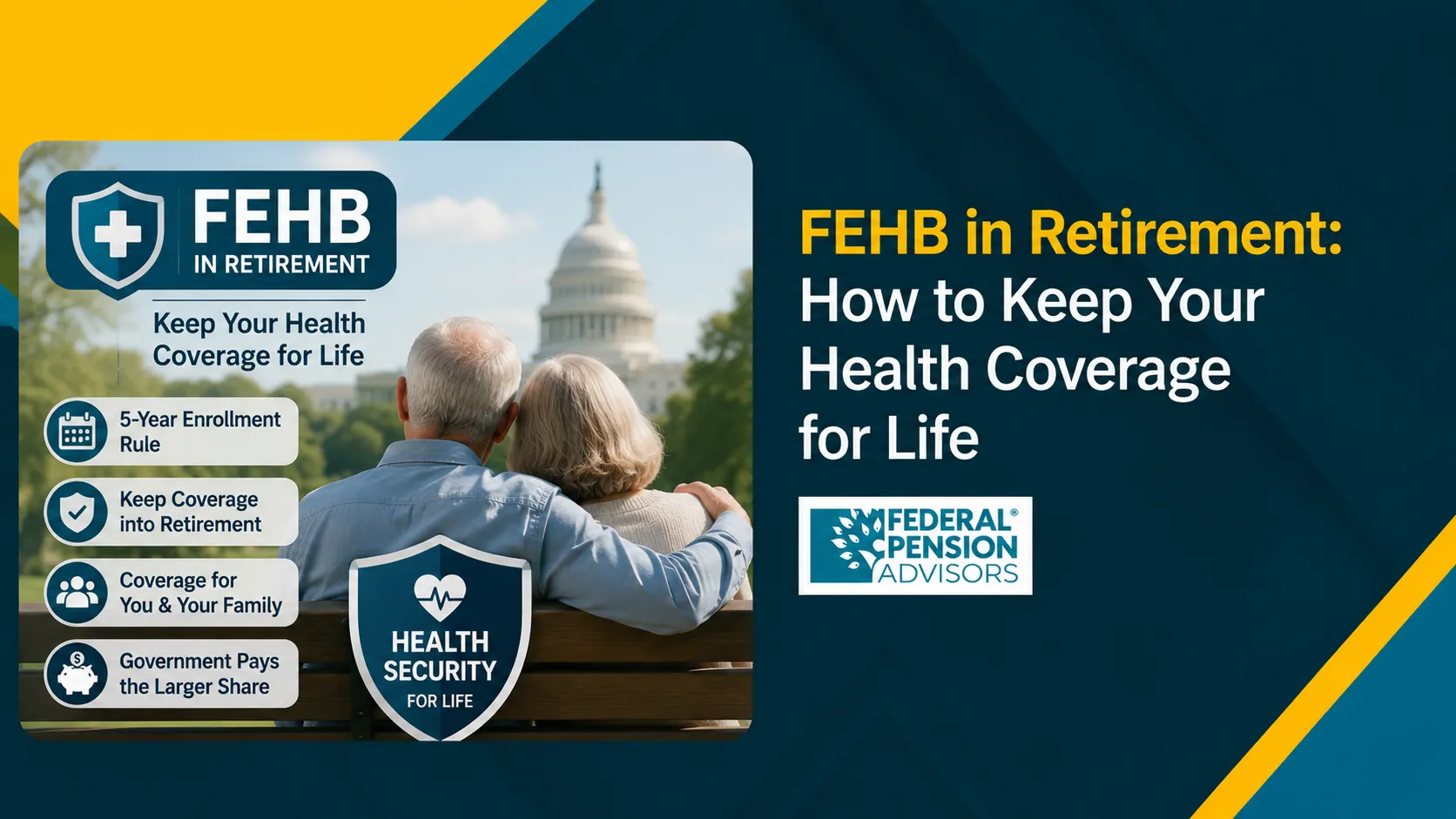

FEHB in Retirement: How to Keep Your Health Coverage for Life

To meet FEHB retirement eligibility, you must retire on an immediate annuity and stay continuously enrolled in the Federal Employees Health Benefits (FEHB) program, the federal government's health insurance system, for the five years right before your annuity begins. If your service is shorter, you must have been covered for your entire period of service since your first chance to enroll.

Meet both conditions, and you can generally keep FEHB coverage for life, as long as you remain eligible and enrolled. The government keeps paying the larger share of your premium.

Miss them, and you may lose the ability to carry one of the most valuable benefits in federal service into retirement.

This guide explains how FEHB retirement eligibility works. You'll learn what the five-year rule does and does not require, how premiums change once you retire, how FEHB coordinates with Medicare, and what steps to take before you separate from service.

Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, prepared this guide to help you make this decision with confidence.

What FEHB Retirement Eligibility Means

FEHB retirement eligibility is the set of conditions you must satisfy to carry FEHB coverage from active employment into retirement. The rules are specific, and they don't bend for most people.

According to the U.S. Office of Personnel Management (OPM), the agency that administers federal benefits, you qualify only if two things are true. You must be entitled to retire on an immediate annuity. And you must have been continuously enrolled in any FEHB plan for the five years of service right before your annuity start date.

Served fewer than five years since your first chance to enroll? Then you must have been covered for that entire period instead.

These rules apply whether you retire under the Federal Employees Retirement System (FERS), which covers employees hired after 1983, or the older Civil Service Retirement System (CSRS).

The FEHB Five-Year Rule Explained

The FEHB five-year rule is the single most important requirement for keeping your coverage in retirement. You must have been enrolled in FEHB continuously for the five years right before you retire, or for your entire period of service since you first became eligible.

The rule measures coverage, not a specific plan. This distinction matters more than most people realize.

You keep your eligibility even if you change plans, switch carriers, or adjust your enrollment type during those five years. OPM doesn't care if you switched providers under the FEHB umbrella during that time. Moving between Self Only, Self Plus One, and Self and Family enrollment has no effect on the rule.

Are you and your spouse both federal employees? Then being covered as a family member under your spouse's enrollment also counts.

For a deeper look at who can stay covered under your enrollment, see our guide to FEHB family member eligibility rules.

TRICARE, the military health program, can count toward the five years, as long as you were enrolled in an FEHB plan when you retire. A break in federal service won't automatically disqualify you either. The rule looks at the five years of service right before retirement, so prior coverage can count if you could not have held FEHB during the gap.

Here's the critical warning. A gap in qualifying coverage during your final five years can cost you the right to carry FEHB into retirement, unless another qualifying coverage period applies or OPM grants a waiver.

Some employees consider dropping FEHB in their last working years to save money. This is one of the most expensive mistakes a federal employee can make. Once you've left federal service, it generally can't be undone.

Waivers of the Five-Year Rule

OPM holds the authority to waive the five-year requirement. Waivers are uncommon, though, and OPM grants them only in narrow circumstances.

OPM may waive the eligibility requirements when, in its sole discretion, it determines that due to exceptional circumstances it would be against equity and good conscience not to allow a person to be enrolled in the FEHB Program as an annuitant.

To request a waiver, you must show OPM three things. You must provide evidence that you intended to have FEHB coverage as an annuitant, that the circumstances preventing you from meeting the requirements were beyond your control, and that you acted reasonably to protect your right to continue coverage into retirement.

An early retirement offer, a reduction in force, or a buyout authority can support a waiver request. But you should never plan on receiving one.

Don't rely on a waiver. Build your retirement timeline as if the five-year rule must be fully satisfied.

What Happens to Your FEHB Premiums in Retirement

Your share of the FEHB premium doesn't increase simply because you retire. In many plans, retirees pay a share similar to active employees, but the government contribution is capped.

For most employees and annuitants, OPM pays the lesser of 72 percent of the weighted average premium across all FEHB plans or 75 percent of the selected plan's total premium. For higher-cost plans, your share can exceed the 25 to 28 percent range.

According to OPM, employees and retirees generally pay about 25 to 28 percent of FEHB premiums, with the federal government paying roughly 72 to 75 percent. For the 2026 plan year, OPM set the government contribution at 72 percent of the weighted average premium, subject to the 75 percent per-plan cap.

There is one meaningful change. While you're working, your premiums come out pre-tax under the premium conversion program. While still employed, you can also use the Federal Paycheck Calculator to estimate how FEHB premiums affect take-home pay.

In retirement, your share of cost stays the same. But most retirees pay FEHB premiums with after-tax dollars, since annuitants generally aren't eligible for premium conversion.

Eligible retired public safety officers may qualify for a separate federal income tax exclusion for certain health insurance premiums, commonly up to $3,000. This is not the same as active-employee premium conversion.

In retirement, OPM deducts your premiums automatically from your monthly annuity once it finalizes your pension. During the interim period before finalization, you'll receive bills from BENEFEDS. Pay them promptly to avoid a lapse.

FEHB premiums: active employee vs. retiree

Source: U.S. Office of Personnel Management (OPM), 2026 FEHB program data.

FEHB and Medicare in Retirement

Once you reach age 65, FEHB coordinates with Medicare, the federal health insurance program for people 65 and older. Most federal retirees enroll in Medicare Part A, which is premium-free for those who paid Medicare taxes during their careers.

The bigger decision is Medicare Part B, which carries a monthly premium. According to the Centers for Medicare & Medicaid Services (CMS), the standard Medicare Part B premium is $202.90 per month in 2026. Higher-income retirees may pay more because of the Income-Related Monthly Adjustment Amount (IRMAA).

You're not required to take Part B to keep FEHB. FEHB can remain substantial coverage on its own.

The value of adding Part B depends on your specific FEHB plan, expected care needs, and premium costs. This depends entirely on your situation, which is why it's worth modeling carefully.

Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, regularly helps clients weigh the trade-offs of adding Part B against the extra premium cost.

Protecting FEHB for Your Surviving Spouse

Keeping FEHB for life is not only about your own coverage. It's also about what happens to your spouse.

If you're the enrollee and you die, your spouse can continue FEHB only if you elected a survivor annuity on your retirement application. Your spouse must also be covered under your FEHB enrollment at the time of your death, typically a Self Plus One or Self and Family enrollment.

Choose the full 50 percent or partial 25 percent survivor benefit, and you preserve your spouse's eligibility for FEHB after your death. Without a survivor annuity, a non-federal spouse loses FEHB coverage when you die, unless that spouse qualifies for FEHB independently as a federal employee or retiree.

This is a permanent, irreversible election made at retirement. It deserves careful thought before you submit your paperwork.

Steps to Secure Your FEHB Before You Retire

Follow these steps in order to protect your eligibility and avoid the most common pitfalls.

- Confirm your enrollment history. Verify that you've been continuously covered under FEHB, under your own or a family member's enrollment, for the five years right before your planned retirement date.

- Confirm your immediate annuity. Make sure you're retiring on an immediate annuity, including under the FERS Minimum Retirement Age (MRA) + 10 provision, which is the earliest age a FERS employee can retire with an immediate annuity combined with at least 10 years of service.

- Don't drop coverage to save money. Keep FEHB through your final working years. A gap in qualifying coverage can cost you the right to carry FEHB into retirement.

- Decide on a survivor annuity. If you're married, plan your survivor benefit election to preserve your spouse's future FEHB access.

- Plan for Medicare at 65. Model whether Medicare Part B makes sense alongside your FEHB plan.

- Verify figures against official sources. Check current premiums and contribution amounts in the annual OPM premium tables before you finalize decisions.

The Bottom Line

FEHB is among the most valuable benefits a federal career offers, and you can keep it for life. But only if you satisfy FEHB retirement eligibility before you separate.

Retire on an immediate annuity. Stay continuously enrolled for your final five years. Protect your spouse with a survivor election, and plan ahead for Medicare.

Each of these decisions is permanent once you retire. That's why getting them right the first time matters so much.

Federal Pension Advisors, a retirement planning firm specializing in federal employee benefits, helps you verify your eligibility, understand premium and Medicare costs, and time your retirement to lock in lifetime coverage. Schedule a consultation with Federal Pension Advisors to review how FEHB, Medicare, survivor benefits, and retirement timing may affect your situation.

Frequently Asked Questions

What are the eligibility requirements to keep FEHB in retirement?

To keep FEHB in retirement, you must retire on an immediate annuity and stay continuously enrolled in any FEHB plan for the five years right before your annuity begins. Have fewer than five years of service since first eligibility? Then you must have been covered the entire time, according to OPM.

How long do I have to have FEHB before I can retire with it?

You must be continuously enrolled in FEHB for the five years right before your retirement, according to the U.S. Office of Personnel Management. You may switch plans or carriers during those years. But a gap in qualifying coverage can cost you eligibility to carry FEHB into retirement, unless a waiver or other qualifying coverage applies.

Do my FEHB premiums increase when I retire?

No. Your share is generally similar to what active employees pay, but it varies by plan because the government contribution is capped, according to OPM. The main change: OPM deducts your premiums from your monthly annuity and, for most retirees, you pay them with after-tax dollars instead of pre-tax.

Can I get FEHB back after retirement if I dropped it?

No. Annuitants who aren't enrolled in FEHB at retirement can't enroll afterward. If you cancel or have a gap in qualifying coverage during the five years before you retire, you can lose the right to carry FEHB into retirement. OPM waivers for this rule are granted only in limited circumstances.

What happens to my FEHB when I turn 65 and have Medicare?

At 65 you can keep FEHB and add Medicare. Most retirees take premium-free Part A. Part B is optional and carries a standard premium of $202.90 per month in 2026, according to CMS. Whether adding Part B is worthwhile depends on your FEHB plan, care needs, and budget.

Can my spouse keep FEHB after I die?

Your spouse can keep FEHB after your death only if you elected a survivor annuity on your retirement application and your spouse was covered under your FEHB enrollment at the time of your death. Without a survivor annuity, a non-federal spouse loses FEHB coverage when you die, unless they qualify for FEHB on their own.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, tax, Medicare, or federal benefits advice. FEHB, Medicare, and retirement rules may change. Verify all figures and eligibility requirements with OPM, CMS, and other official sources before making retirement decisions.

Get Updated

Subscribe to our weekly updates for the latest on retirement planning, federal benefits, exclusive webinars, and more!

Thomas A. Doherty

Thomas A. Doherty is a retirement planning consultant with 35 years of experience helping federal employees understand and maximize their retirement benefits. His expertise includes FERS retirement planning, pension strategies, federal benefits, retirement income planning, and tax-efficient retirement decisions. Thomas specializes in helping federal employees navigate complex retirement rules, including the FERS annuity, Special Retirement Supplement, FEHB, and long-term income planning.

Download Federal Retirement: Step-by-step Checklist

This comprehensive guide will help you understand your federal benefits, optimize your savings, and plan for a comfortable future.